When debt becomes unmanageable—especially during a financial emergency—the fear of Bank Harassment and the stress of mounting debt can be crippling. A Loan Settlement (often called One-Time Settlement or OTS) is a strategic, definitive way to end the debt and the harassment simultaneously.

A settlement is a formal agreement where your bank agrees to accept a reduced, one-time payment to close your loan account as full and final satisfaction. It’s a tool for financial recovery when all other repayment options are exhausted.

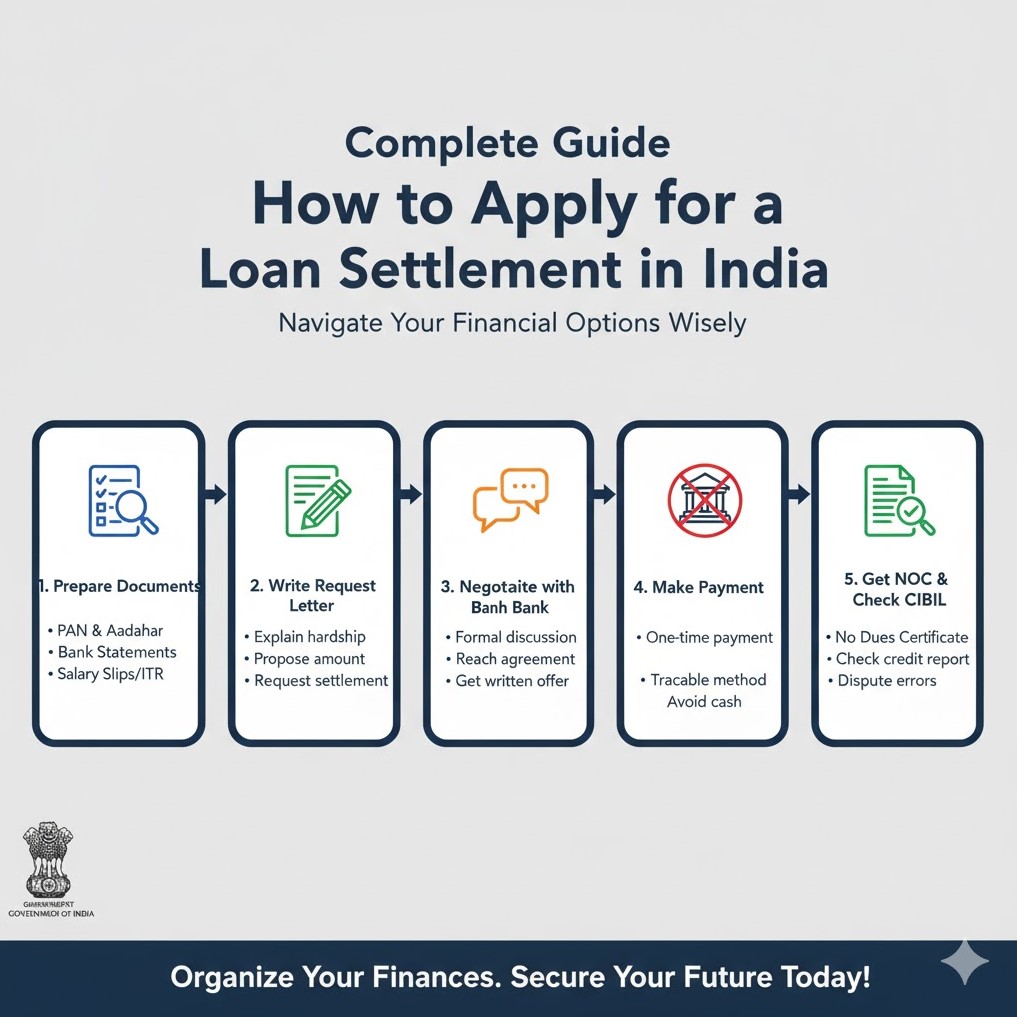

This borrower guide details the steps to initiate and successfully complete a settlement, protecting your rights throughout the bank process.

Step 1: Self-Assessment and Eligibility Check

Loan settlement should be your last resort. Lenders usually consider it only when they classify the loan as a Non-Performing Asset (NPA).

-

Eligibility: Your loan must typically be in default for 6 months or more and classified as an NPA. Banks use settlement to recover at least a partial amount from a loan they consider highly unlikely to be fully repaid.

-

Determine Your Capacity: Calculate the maximum lump sum amount you can realistically afford to pay right now (from savings, selling minor assets, or family help). Your initial negotiation offer should be based on this capacity (typically start by offering 40-50% of the outstanding principal).

-

Gather Hardship Documents: The bank will only negotiate if you demonstrate genuine, verifiable financial distress. Prepare documentation:

-

Proof of Financial Hardship: Job termination letter, severe medical bills, proof of business closure/loss, etc.

-

Financial Records: Last 6-12 months’ bank statements, latest Income Tax Returns (ITR).

-

Step 2: Formal Communication and Application

Do not wait for the recovery agent to make the first move. Initiate the formal request yourself to gain control.

-

Approach the Right Channel: Bypass the aggressive recovery agents. Send your formal request to the bank’s Grievance Redressal Officer (GRO) or the Head of the Legal/Collections Department. Their contact details are mandatory on the bank’s website.

-

Submit Written Request: Write a formal application letter requesting an OTS.

-

Clearly state the loan account number.

-

Briefly explain the cause of your genuine financial hardship.

-

Propose your calculated settlement amount.

-

Attach the hardship documentation.

-

-

Document Harassment: If you are experiencing Bank Harassment (calls outside 7 AM–7 PM, abusive language), document these violations and mention in your letter that you expect all future communication to be routed through formal channels only, citing the RBI Fair Practices Code.

Step 3: The Negotiation and Agreement

Negotiation is a formal business process. The bank’s goal is to maximize recovery; your goal is to minimize your payout while achieving a debt-free status.

-

Negotiate Realistically: The bank’s counter-offer will likely be higher than your proposal (often landing between 55-70% of the outstanding principal). Be prepared to negotiate back and forth, firmly stating that your offer is the maximum you can pay as a lump sum.

-

Focus on Lump Sum (OTS): Banks strongly prefer a lump-sum payment as it closes the account immediately, reducing their risk. If a lump sum is impossible, negotiate a very short, time-bound installment plan (e.g., 2-3 months).

-

Obtain the Formal Settlement Letter: Never make any payment based on a verbal promise. Once you have a final agreed amount, demand a Loan Settlement Letter on the bank’s official letterhead.

-

This letter must state the final agreed amount, the payment deadline, and confirm that this payment will be accepted as full and final satisfaction of the loan, with the remaining balance being waived.

-

The letter must also promise the issuance of a No Dues Certificate (NDC) after payment.

-

Step 4: Final Payment and Documentation

This is the most critical step that makes you debt free and permanently stops all collection activity.

-

Make the Payment: Pay the agreed lump sum amount strictly before the deadline stated in the settlement letter. Keep every receipt and transaction record.

-

Collect the NDC: Follow up immediately to ensure you receive the No Dues Certificate (NDC). This is the most important document—it is your legal proof that the debt is closed forever.

Step 5: Post-Settlement Credit Monitoring

A settlement is reported negatively to credit bureaus, but you must ensure it is reported correctly.

-

Check Status: Within 45-60 days, check your CIBIL/Credit Report. The account must be marked “Settled” and not “Written-Off” or “Defaulted.” A “Settled” status is better for your future financial recovery.

-

Dispute Errors: If the status is incorrect, immediately raise a dispute with the credit bureau and the bank, providing the Loan Settlement Letter and NDC as evidence.

By following this controlled, documented process, you achieve not only debt relief but also gain the necessary Legal Support to shut down any further Bank Harassment.