You’ve done the hard work: you negotiated the deal, paid the final amount, and closed a stressful chapter. Congratulations! Achieving a Loan Settlement is a massive win for debt closure and signals the immediate end of Bank Harassment and the start of your financial planning for the future.

But what exactly happens next? The settlement process isn’t truly finished until you’ve secured the final documents and understood the necessary steps for post-settlement financial recovery.

Here is a comprehensive guide to the critical actions you must take immediately after your payment clears.

1. The Most Critical Step: Secure the Debt Closure Documents

Your first and most important action is securing the legal proof that your debt is closed. This documentation is your shield against any future claims or continued harassment.

-

The No Dues Certificate (NDC): This is the most crucial document. The NDC is a legal paper issued by the bank confirming that, after receiving the settlement amount, you have zero remaining liability on the loan account. Keep this document safely forever.

-

The Settlement Letter: Retain the original Loan Settlement Letter (the one stating the agreed final amount). You need this to cross-reference the payment and the NDC.

-

Payment Proof: Keep all bank receipts or transaction confirmations for the final settlement amount paid.

Why it matters: These documents permanently stop the bank or any third-party collection agency from claiming any further amount or engaging in any further recovery activity, including Bank Harassment.

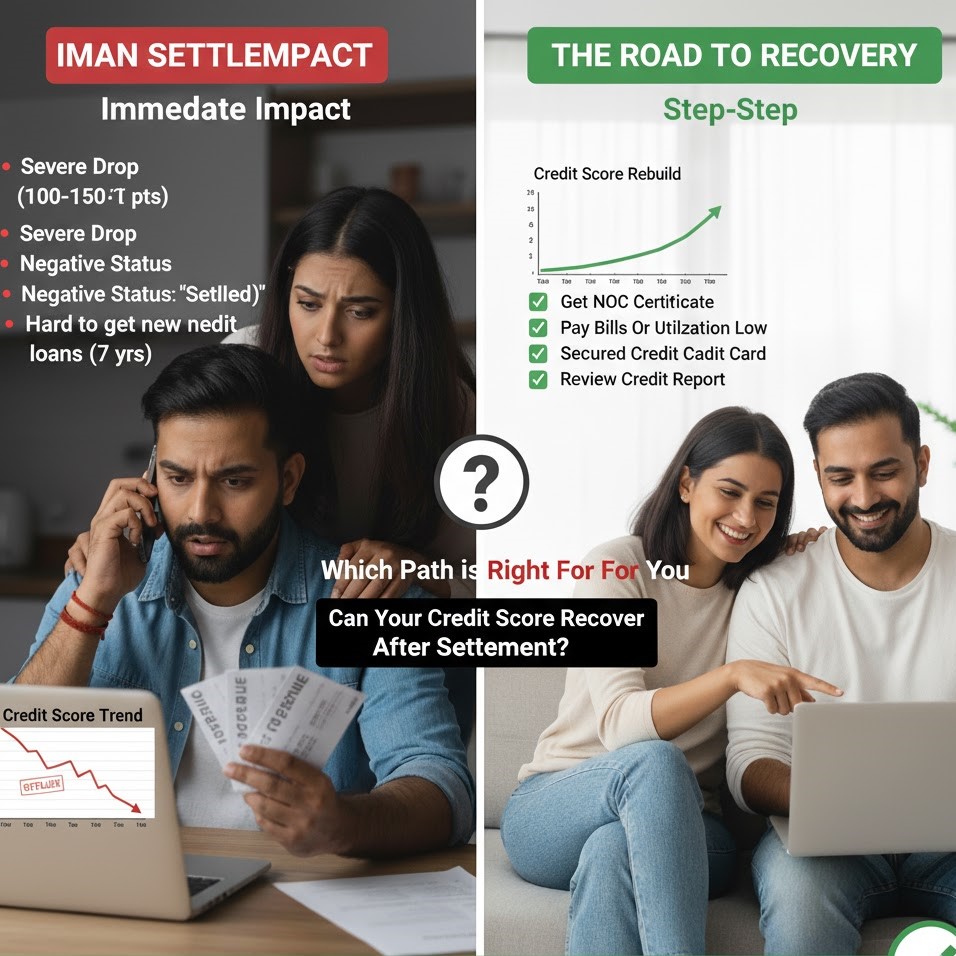

2. Monitoring and Repairing Your Credit Score

A settled loan means the debt is gone, but the status is reflected negatively on your credit report. You must monitor this closely.

-

Check the Status: Within 45–60 days of settlement, pull your credit report (CIBIL, Experian, etc.). Ensure the loan account status is correctly marked as “Settled” and not “Default,” “Written-Off,” or “Closed.”

-

Correcting Errors: If the bank has misreported the status, immediately raise a dispute with the credit bureau and the bank, providing copies of your Loan Settlement Letter and NDC as proof. This step is vital for your long-term financial recovery.

-

Credit Impact: The “Settled” status will affect your credit score for up to seven years. Acknowledge this, but remember that a closed, settled account is always better than an open, perpetually defaulting one that invites constant harassment.

3. Addressing Tax Implications (Consult a CA)

In India, the amount of debt waived by the lender may be treated as “Income from Other Sources” under the Income Tax Act.

-

The Waived Amount: The difference between the original outstanding debt and the final settlement amount is the “waived” debt.

-

Tax Expert: Consult a Chartered Accountant (CA) to determine if the waived amount is taxable for you and how to correctly report the settlement on your tax returns for the relevant financial year. Do not wait for the Income Tax Department to send a notice.

4. Starting Your New Financial Planning Chapter

With the debt closed, you can finally focus your energy and cash flow on building a secure future, free from the stress of Bank Harassment.

-

Reallocate Funds: Re-direct the money previously intended for EMIs or collections into savings or investment vehicles.

-

Build an Emergency Fund: Your first financial priority should be building an emergency fund covering 3–6 months of essential living expenses. A large debt often started because an emergency couldn’t be covered.

-

Responsible Credit Use: If you still have other credit lines (like a credit card), use them sparingly and pay the full balance on time every month to start rebuilding a positive payment history immediately.

A successful Loan Settlement is an end, but also a new beginning. By handling the paperwork correctly and committing to smart financial planning, you ensure that the settled debt truly paves the way for lasting financial stability.

Need help checking your credit report post-settlement?

Contact Us today to ensure your debt closure is reported correctly and securely.