Credit card loan settlement often feels like a life raft when you’re drowning in debt. It provides immediate relief, but what most people don’t fully realize is the long-term shadow it casts over their financial future, especially regarding new loan approvals.

If you’ve opted for a settlement, you’ve taken a crucial step toward debt relief. Now, you need to understand the lasting effects and, more importantly, know your rights against aggressive collection tactics, which too often cross the line into Bank Harassment.

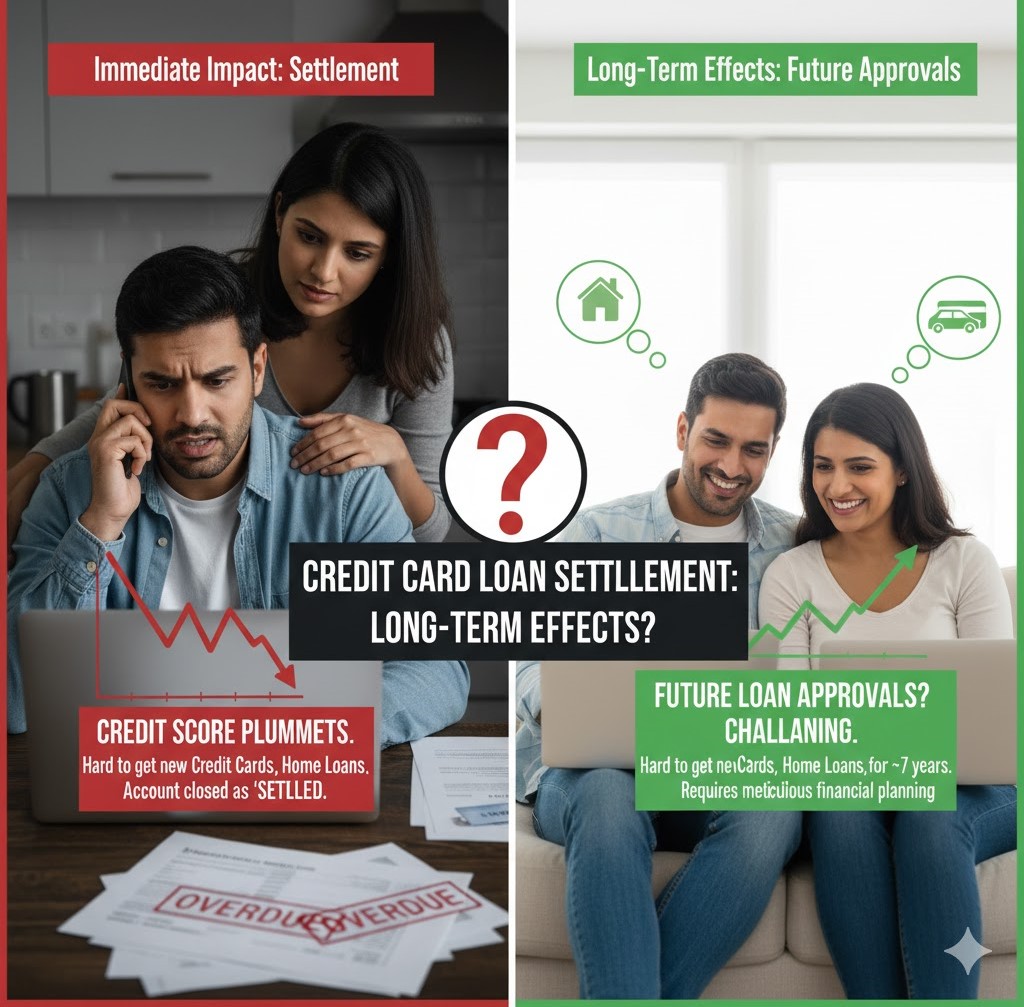

The Lingering Mark on Your Credit Score

Loan settlement is a double-edged sword that provides short-term gain but long-term pain for your Credit Score.

- The “Settled” Status: When you settle a loan, the bank accepts less than the full amount owed. On your credit report, this account is marked as “Settled,” not “Closed” or “Paid in Full.” This single word is a significant red flag for future lenders, indicating you were unable to meet your full financial obligation.

- The Score Drop: The act of settling causes a substantial and immediate drop in your credit score, often by 75 to 150 points or more.

- The 7-Year Hangover: The “Settled” status remains visible on your credit report for up to seven years. Even if you make timely payments on other debts, this negative mark severely impacts how lenders view your creditworthiness for years to come.

Impact on Future Loan Approvals

The consequences of a settled loan on your future borrowing capacity are profound:

- Rejections are Common: For up to seven years, banks and financial institutions will view you as a high-risk borrower. This often leads to immediate rejections for major credit products like personal loans, home loans, car loans, and new credit cards.

- Higher Interest Rates: If an approval is granted, it will almost certainly come with significantly higher interest rates and less favourable terms compared to what a borrower with a clean record receives. Lenders price in the higher risk associated with a settled account.

- Stricter Scrutiny: Lenders may demand more documentation, stricter background checks, or even require a guarantor or collateral before extending credit.

Settlement should truly be the last resort after exhausting all other options like loan restructuring or EMI deferment.

🛡️ How to Fight Back Against Bank Harassment 🛡️

A settled loan does NOT give a bank or its agents the right to harass you. If you are facing aggressive, disrespectful, or threatening collection calls, remember you have rights under the law and guidelines set by the RBI.

- Know the Rules: Recovery agents are only permitted to Contact Us between 7:00 AM and 7:00 PM on working days. They must maintain a respectful demeanor, identify themselves, and cannot publicly humiliate you.

- Document Everything: Keep a detailed log of every instance of Bank Harassment. Note the date, time, agent’s name, agency name, and the exact nature of the communication (e.g., threatening language, calls outside of hours, calls to family/workplace).

- File a Formal Complaint:

- Bank’s Grievance Cell: File a formal complaint with the bank’s internal grievance redressal mechanism first.

- RBI Ombudsman: If the bank fails to resolve your complaint within 30 days, escalate the matter to the RBI Integrated Ombudsman Scheme (RB-IOS). This is a powerful, free mechanism for resolving customer complaints.

Don’t let debt turn into an ordeal. Know your rights, protect your financial future, and stand up to Bank Harassment.

If you need help understanding the long-term impact on your credit report or require assistance in fighting back against illegal collection tactics, Contact Us today.