The road to debt relief is often paved with stress, fear, and relentless bank harassment. If you’ve reached the point where a credit card loan settlement seems like the only escape, you need a powerful strategy.

A successful negotiation can stop the calls, reduce your debt, and return control to you. At Bank Harassment, we focus on empowering you through this process.

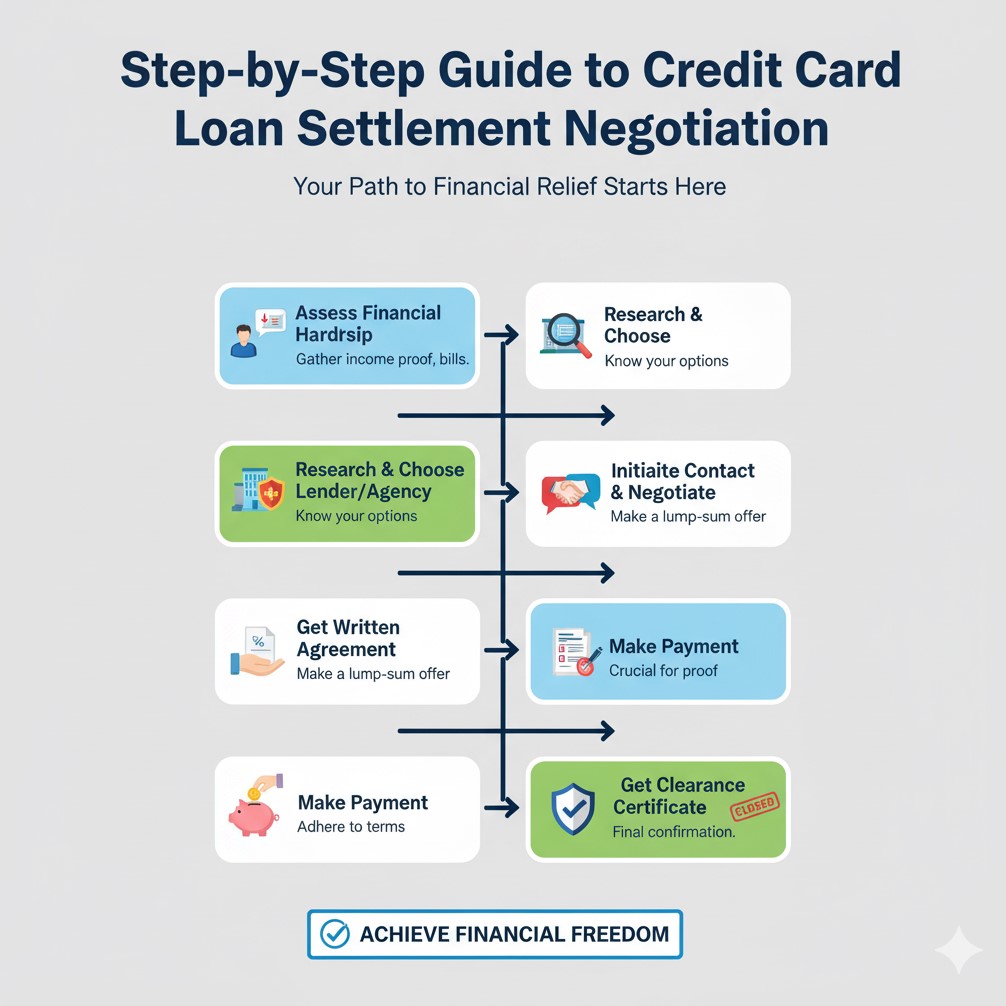

Here is your essential, step-by-step guide to mastering the credit card loan settlement negotiation.

Step 1: Prepare Your Ground – Know Your Leverage

Your negotiation power is built before you even talk to the bank.

- The ‘Financial Hardship’ Evidence: A settlement is a business decision for the bank. They only agree if they believe they will lose more money trying to collect than by settling. Gather evidence of your financial hardship (job loss letter, medical bills, reduced income proof). This justifies your need for debt relief.

- Determine Your Funds (The Lump Sum): Banks overwhelmingly prefer a one-time, lump-sum payment. Determine the absolute maximum amount of cash you can realistically raise. Your ability to offer a chunk of money quickly is your biggest negotiation tip.

- Understand the Harassment Rule: Document all instances of bank harassment. If an agent is unethical, your legal partner can use this misconduct as leverage during the settlement process.

Step 2: Establish Professional Communication

Do not deal with the entry-level collection agents who are focused only on targets.

- Go to the Source: Insist on dealing directly with the bank’s Recovery, Write-Off, or Settlement Department. These are the only personnel authorized to approve deep discounts.

- Engage a Partner (Recommended): If you are facing severe bank harassment, engaging a professional debt resolution partner allows you to step away. We will formally direct all bank communication to contact us directly, creating a shield that stops the daily calls and emotional abuse immediately.

- Make the First Offer: If you are negotiating directly, offer a number you are comfortable with—but start low (e.g., 25%-30% of the total outstanding amount). This sets the lower boundary for the negotiation.

Step 3: Master the Negotiation Tactics

The process involves back-and-forth, but a firm, realistic position is key.

- Focus on the Principal: Your main goal is to get the bank to waive penalties, late fees, and accumulated interest. A reasonable settlement is often achieved between 40% and 60% of the total outstanding balance.

- The “Final” Offer Strategy: When you make your final, firm offer, present it as your absolute maximum, non-negotiable lump sum, ready to be paid within a few days. This applies pressure and signals seriousness.

- Do Not Accept Pressure: If the negotiator attempts to use intimidation or revive the agent harassment tactics, calmly reiterate your documented financial hardship and the fact that their offer is unaffordable. Do not let them bully you into a higher number.

Step 4: Secure the Written Settlement Agreement (Crucial for Debt Relief)

This is the most critical stage. Do not pay a single rupee until you have this letter.

- Demand Formal Documentation: Once a figure is agreed upon, insist on a formal, written “Settlement Letter” on the bank’s letterhead.

- Verify the Details: The letter must clearly state:

- The original debt amount.

- The final, agreed-upon settlement amount.

- The deadline for payment.

- Confirmation that the account will be considered “Closed” or “Settled” and the remaining balance written off.

Step 5: Final Payment and Peace

Upon payment, you take the final step toward freedom.

- Immediate Payment: Make the agreed payment before the deadline and keep the receipt.

- Obtain the No Dues Certificate (NDC): This is the ultimate proof of debt relief. Within 15-30 days of the payment, the bank is legally required to issue a No Dues Certificate confirming you have no further financial liability. This NDC makes any future collection effort or bank harassment against that account illegal and easily defeated.

End the Harassment, Achieve Relief

A credit card loan settlement is a tool for smart, decisive debt relief. When backed by strategic negotiation tips, it’s your most effective defense against bank harassment.

Ready to take control? Contact Us at Bank Harassment for expert guidance and to find the right path to peace and financial freedom.