Facing overwhelming debt and struggling to maintain your EMI payments can feel hopeless, especially when compounded by relentless Bank Harassment. However, for defaulted loans, debt settlement is a strategic and legal option that provides significant EMI relief and a definitive path to debt closure and peace of mind.

Debt settlement is a negotiation process where the bank agrees to accept a single, reduced lump sum payment that is less than the total outstanding amount, thereby waiving the remainder of the debt.

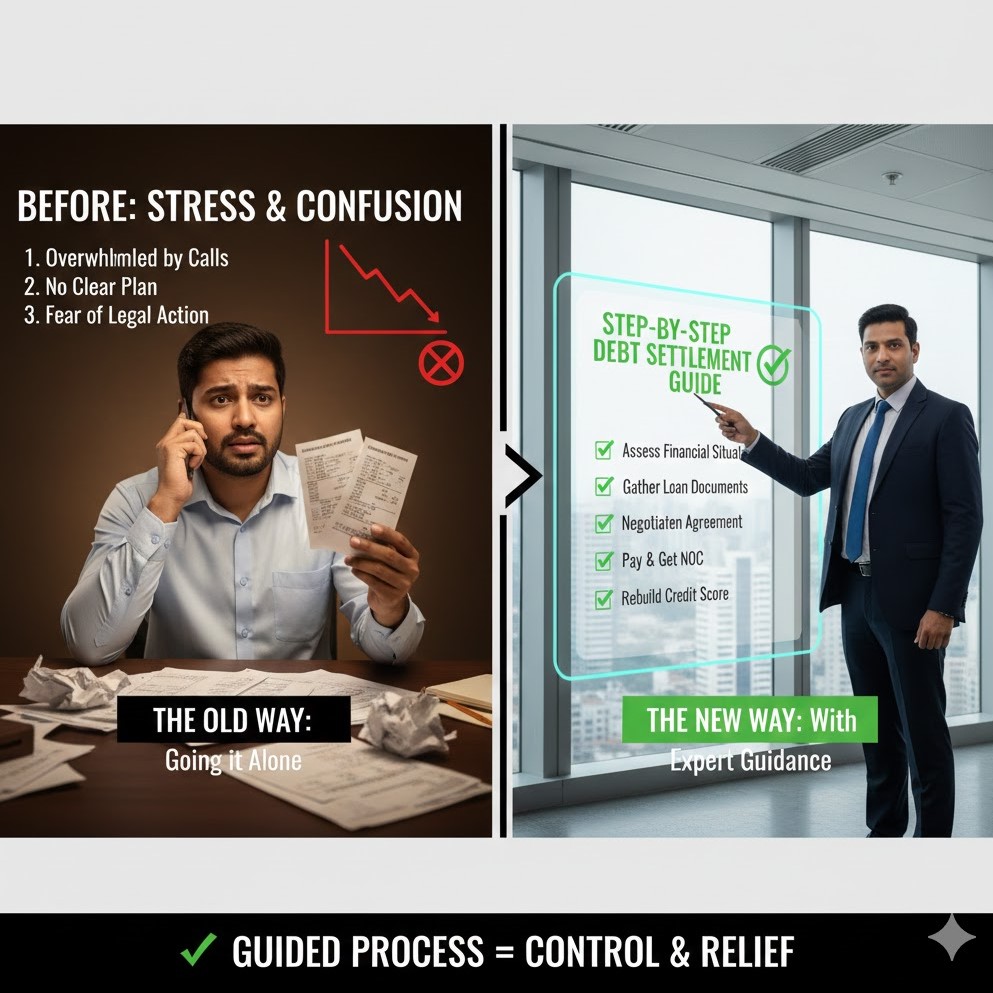

Here is a comprehensive, step-by-step guide tailored for Indian borrowers to navigate the repayment process, stop harassment, and achieve a successful settlement.

Step 1: Acknowledge Default, Document Harassment, and Assess Financial Status

You must act decisively the moment you realize your current repayment process is permanently unsustainable.

-

Document Harassment: Start a log immediately. Note the date, time, agent’s name, phone number, and the exact abusive/threatening language used. This evidence is crucial leverage.

-

Determine Your Capacity: Calculate the exact lump sum amount you can realistically afford to pay right now (your settlement offer). This is your absolute maximum.

-

Gather Hardship Proof: Secure all necessary proof of genuine financial hardship (e.g., job loss letter, medical records, documented salary cut). Banks require this evidence to justify the debt waiver.

Step 2: Understanding the Negotiation Window and Initiate Complaint

Timing and legal protection are key to a successful outcome.

-

NPA Status: Banks only seriously consider debt settlement when the loan is classified as a Non-Performing Asset (NPA), typically 90+ days overdue.

-

Initiate Legal Complaint: File a formal written complaint about the harassment with the bank’s Grievance Redressal Officer (GRO). If the harassment continues, escalate it to the RBI Integrated Ombudsman Scheme (RB-IOS). This forces the bank to treat your file seriously and professionally.

-

Initiate Contact Professionally: Contact the bank’s Legal/Collections Head or GRO (not the field agent). Express your inability to pay and state your intent to seek a formal One-Time Settlement (OTS).

Step 3: Submitting the Formal Settlement Offer (The Strategy)

Your offer must be professional, factual, and backed by your capacity to pay.

-

Draft the Letter: Prepare a formal Loan Settlement Letter (OTS request). Clearly state your loan account number, explain the verified financial hardship, and propose a specific lump sum settlement value.

-

Request the Waiver: Explicitly request the waiver of all accumulated penalties, late fees, and remaining interest.

-

Demand Written Agreement: State clearly that your offer is conditional upon receiving a formal Loan Settlement Letter from the bank on their letterhead before you make the final payment. Never pay based on a verbal promise.

Step 4: Negotiate, Finalize, and Pay (The Closure)

Expect the bank to counter-offer. Maintain a firm, professional stance.

-

The Counter: The bank will counter-offer, typically higher than your initial proposal. Use your lump-sum capacity and the leverage of your formal harassment complaints to push the final figure down to a manageable level.

-

Secure the Settlement Letter: Once a final amount is agreed upon, do not pay until you have the official, signed Loan Settlement Letter. Verify that the letter clearly states the payment is accepted as “full and final satisfaction” of the debt.

-

Final Payment: Pay the exact agreed-upon lump sum by the deadline specified in the letter.

Step 5: Post-Settlement Due Diligence (The Debt Closure)

Your debt is not legally closed, and the threat of future harassment is not neutralized, until you have the final documents.

-

Collect the NDC: Immediately follow up to obtain the No Dues Certificate (NDC). This legal document is your irrefutable proof of debt closure and permanent EMI relief. Keep this document forever.

-

Monitor Credit Report: Within 60 days, check your CIBIL report. Ensure the status is correctly marked “Settled” (not “Written-Off”). Dispute any errors using your NDC.

-

New Financial Plan: The debt is closed, and the harassment is over. Focus your energy on building an emergency fund and consistently maintaining a positive repayment process on any future or existing debts.

By following this disciplined, step-by-step debt settlement guide, Indian borrowers can regain control, secure significant EMI relief, and successfully achieve debt closure free from the stress of Bank Harassment.

Need help structuring your offer and stopping harassment?

Contact Us today for expert guidance on structuring your offer and securing your debt settlement.