Navigating financial distress can be one of the most stressful experiences of your life. When you are unable to keep up with your Personal Loan EMIs, a personal loan settlement often seems like the only escape. While it provides immediate relief from debt and the constant threat of recovery agents, it is a solution with significant, long-lasting consequences for your financial future, particularly your CIBIL score.

At Bank Harassment, we believe every borrower has the right to understand the full picture. More importantly, you have rights against illegal recovery practices, even when your loan is settled.

The Harsh Truth: Personal Loan Settlement vs. Loan Closure

Many borrowers mistakenly believe that a settlement is the same as successfully closing a loan. It is not.

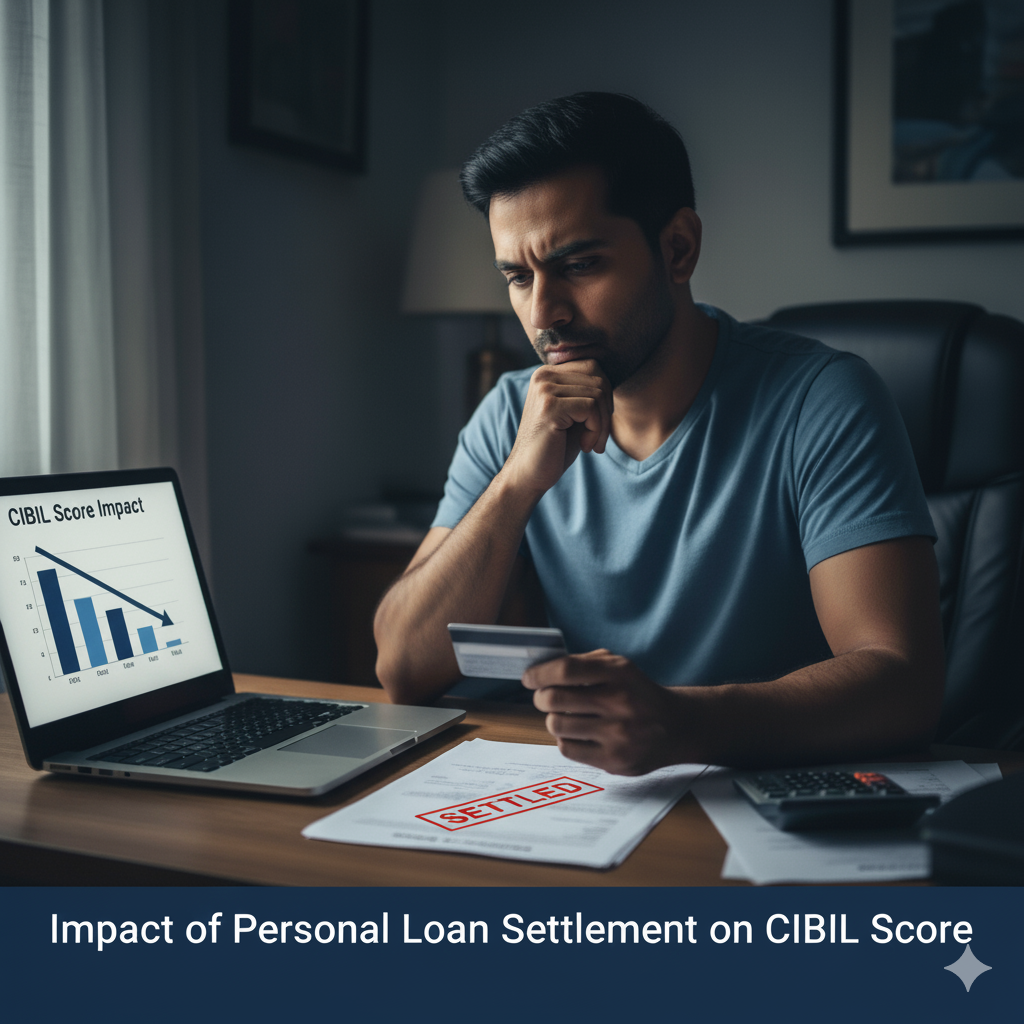

The Immediate Impact on Your CIBIL Score

When your lender reports a personal loan settlement to the Credit Information Bureau (India) Limited (CIBIL), your credit score can drop significantly—often by 50 to 150 points or more.

The “Settled” status is a red flag to future lenders. It signals that you are a high-risk borrower who defaulted on the original terms. This makes getting a new loan, a credit card, or even a home loan extremely difficult for years, and any credit you do receive is likely to come with much higher interest rates.

Are You Still Facing Bank Harassment After Settlement? Know Your Rights!

The irony is that even after you have settled your loan and closed the chapter on your debt, you may still face undue stress or the continuation of aggressive tactics from recovery agents regarding the small, remaining ‘written-off’ amount, documentation, or other matters.

Remember: Harassment is ILLEGAL, regardless of your credit status.

The Reserve Bank of India (RBI) has strict guidelines for debt recovery. If you are experiencing any of the following, you are a victim of Bank Harassment:

- Calls at Odd Hours: Recovery calls must be restricted to between 7:00 AM and 7:00 PM.

- Abusive Language or Threats: Threats of legal action, violence, or using derogatory language are strictly prohibited.

- Public Humiliation: Sharing your debt information with neighbours, employers, or family members.

- Unauthorised Visits: Visiting your workplace or residence without prior appointment and using intimidating behaviour.

Actionable Steps to Stop the Harassment

Do not suffer in silence. Take immediate, documented action:

- Document Everything: Keep a log of every harassing call (date, time, caller name, agency, conversation summary). Save all text messages, emails, or letters.

- Escalate to the Bank: File a formal written complaint with your bank’s designated Grievance Redressal Officer and get an acknowledgement. Refer to the RBI guidelines in your complaint.

- Approach the Banking Ombudsman: If the bank fails to resolve your complaint within 30 days, you can escalate the issue to the Banking Ombudsman, an independent authority appointed by the RBI.

- File a Police Complaint: In cases of physical threats or illegal trespass, do not hesitate to file a police complaint (FIR) against the recovery agent and the bank/NBFC.

Can You Fix Your CIBIL Score After Settlement?

While the “Settled” status remains for up to seven years, you can take steps to mitigate the damage and begin rebuilding your credit profile:

- Pay the Remaining Dues: The most effective step is to contact the lender and ask for the exact remaining principal amount that was written off. Pay this balance immediately.

- Demand an NOC (No-Objection Certificate): Once the remaining amount is paid, demand a “No Dues Certificate” from the bank. Use this document to request that the lender update your status with CIBIL from “Settled” to “Closed.” This can instantly boost your score.

- Practice Perfect Credit Behaviour: Pay all other loans and credit card bills on time, every time. Keep your credit utilisation low (ideally below 30%).

Need Help Dealing with Bank Harassment?

You are not alone. Facing a low credit score while being pursued by aggressive recovery agents is a dual battle. Our mission at Bank Harassment is to provide you with the legal support and resources you need to enforce your rights and stop illegal recovery practices.

Don’t let a settled loan become a source of unending stress.