You did it. You fought the system, secured a loan settlement, and finally put an end to the crushing debt and the abusive Bank Harassment. That is a monumental achievement and the foundation of your financial recovery.

However, the final chapter of your comeback involves repairing the damage to your credit score (your CIBIL score). While the loan settlement leaves a “Settled” mark, you now have a clean slate to build a powerful new financial reputation.

At Bank Harassment, we specialize in turning crisis into control. Here is the step-by-step credit score builder strategy to ensure your financial recovery is swift and complete.

Step 1: Clean the Slate – Use the Law to Verify Your Report

The first step in recovery is ensuring the lender correctly reports the settlement. After the stress of Bank Harassment, banks are often sloppy or deliberately misleading in their final reporting.

A. Secure the No Dues Certificate (NDC)

Upon final payment of the loan settlement amount, demand and keep the official NDC. This document is your ultimate shield against future claims and necessary for credit reporting disputes.

B. Verify Your Credit Report Status

Check your official credit report immediately. The settled account must read “Settled” with a balance.

- Fight Errors: If the bank reports “Written Off” or “Default,” you have grounds for an immediate dispute. Use the evidence of past Bank Harassment and the NDC to push for accurate reporting. Banks, keen to avoid further legal trouble, will often correct errors quickly. A correct status is the fastest initial credit score builder step.

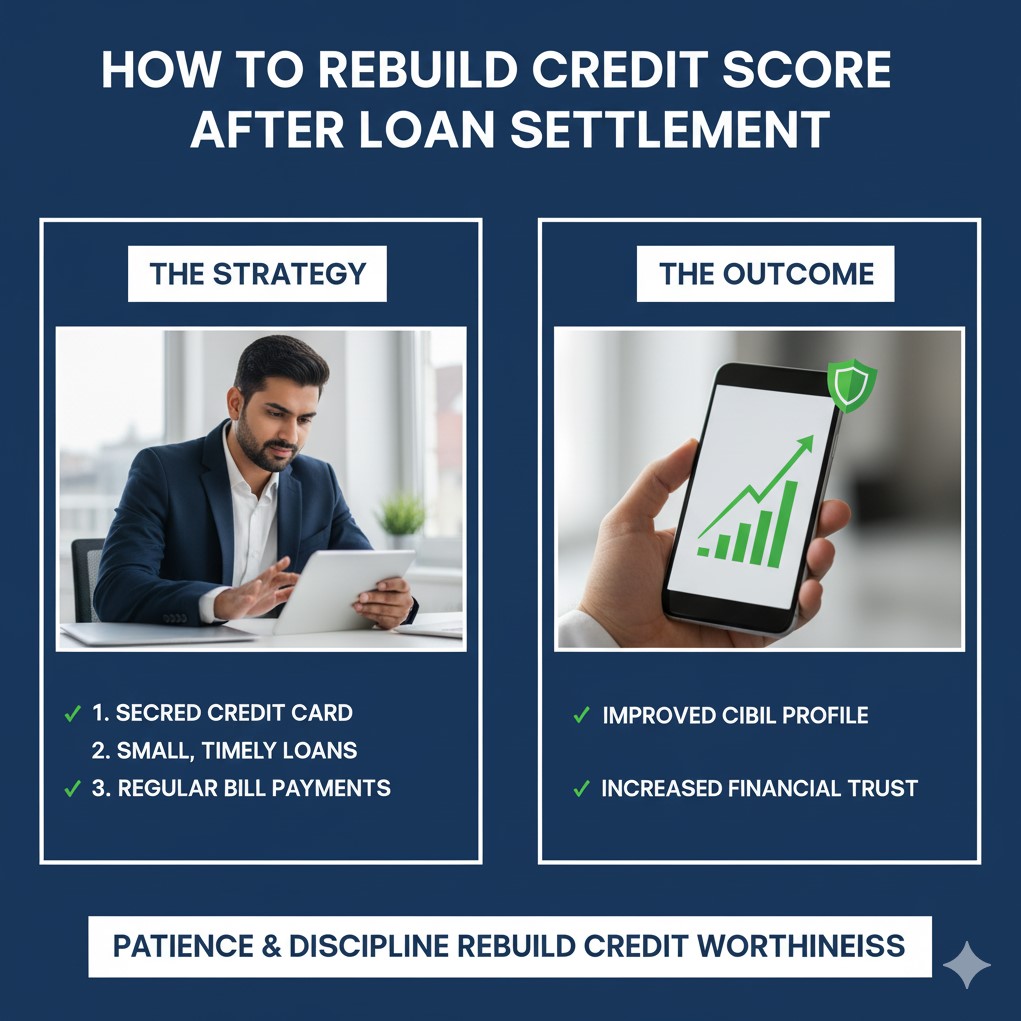

Step 2: Active Recovery – The Credit Score Builder Strategy

Your credit score is built on recent, positive payment history. You must now create this new history to outweigh the negative mark.

A. The Secured Card Strategy: Fast Track Your Recovery

Since obtaining a new unsecured loan or credit card can be difficult post-settlement, your best tool is a secured credit card:

- How it Works: Deposit a small amount ( to ) with a bank and receive a card limit against it.

- The Rule: Use this card for small, manageable expenses and pay the entire bill in full and on time every single month. This flawless repayment history rapidly boosts your score.

B. Zero-Tolerance for Late Payments

Set up auto-pay for every single financial obligation you have—utility bills, rent (if reported), and the new secured card. After a loan settlement, a single late payment is a massive setback. Timely payment is the number one credit score builder factor.

C. Control Your Utilization

On your new secured card, keep your spending low—ideally below of your limit. If your limit is , don’t spend more than . High credit utilization signals financial distress, which negates the positive impact of your on-time payments.

Step 3: Patience – Time Heals All Wounds

The final component of recovery is time. With consistent, perfect payment behavior, the negative impact of the loan settlement will naturally fade. After 2-3 years of a flawless new payment record, lenders will focus on your recent stability, not your past crisis.

Your Final Step to Control

You stopped the Bank Harassment and settled the debt. Now, empower your financial future. Let us guide you through the post-settlement verification and the credit score builder process to ensure your hard-won recovery is complete.