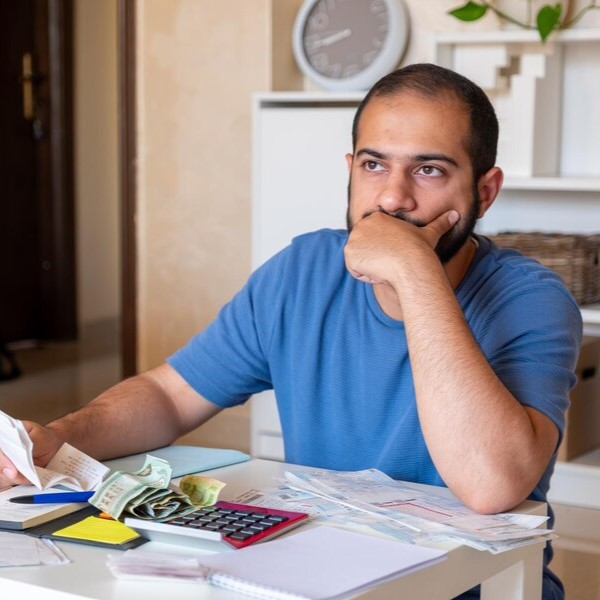

The immediate relief that comes from muting your phone or avoiding unannounced visits from recovery agents is understandable. It feels like a temporary reprieve from the relentless pressure and mental stress. Yet, this silence, when it comes to bank harassment and overdue loans, is often misinterpreted by lenders and can escalate the problem rather than resolve it. Ignoring the issue is rarely a viable long-term strategy for loan default.

At Bank Harassment, we emphasize that proactive action and asserting your borrower rights are crucial. Understanding the potential consequences of ignoring harassment can empower you to engage effectively and achieve peace of mind.

The Illusion of Silence: What Happens When You Ignore Bank Harassment

When you consistently ignore calls and communications from banks or their collection agencies, several things begin to happen:

- Escalation of Tactics:

- Increased Pressure: The silence is often perceived as avoidance, prompting lenders to intensify their debt recovery efforts. This means more frequent calls, potentially from different numbers, and increasingly aggressive tones.

- External Agencies: Your account might be transferred to more persistent or specialized collection agencies, who might use even more stringent (and sometimes illegal) methods.

- Unannounced Visits: Ignoring calls can lead to unannounced visits at your home or workplace, causing immense social embarrassment and mental stress.

- Negative Credit Score Impact:

- Worsening Report: Each missed payment and subsequent non-communication directly impacts your CIBIL score and other credit reports. This leads to a declining score, which remains on your report for years.

- Reduced Future Access: A severely damaged credit score results in credit limitations, making it nearly impossible to get new loans, credit cards, or even rental agreements in the future, affecting your overall financial safety.

- Legal Ramifications:

- Formal Notices: Ignoring initial calls leads to formal demand notices, potentially under the SARFAESI Act for secured loans.

- Legal Action: The bank can initiate legal proceedings. For secured loans, this could mean illegal repossession of your assets (e.g., car, house) if due process is followed. For unsecured loans, they might file a civil suit for recovery, which can lead to court orders for salary attachment or asset seizure.

- Cheque Bounce Cases: If you provided post-dated cheques that bounced, you could face criminal charges under the Negotiable Instruments Act.

- Loss of Negotiation Opportunity:

- Limited Options: By ignoring communication, you shut down any opportunity to negotiate a settlement, restructure your loan, or explain your financial situation. Banks are often more willing to discuss options with borrowers who engage proactively.

- Higher Costs: If the matter goes to court, you could be liable for not just the principal and interest, but also legal fees, adding significantly to your outstanding balance.

- Increased Mental Stress:

- Lingering Anxiety: While ignoring calls provides temporary relief, the underlying problem doesn’t go away. The constant dread of the next call or unexpected visit can prolong and intensify mental stress.

- Isolation: The shame and fear might lead to social withdrawal, exacerbating feelings of isolation.

Why Proactive Action is Your Best Defense

Instead of ignoring bank harassment, proactive engagement is key to protecting your borrower rights and mitigating severe consequences:

- Understand Your Position: First, assess your financial situation and understand the specific loan terms.

- Know Your Rights: Familiarize yourself with RBI Guidelines on debt recovery and what constitutes illegal bank harassment.

- Document Everything: Every call, message, or visit should be meticulously documented. This is your evidence.

- Communicate (Strategically): Respond to the bank, but insist on written communication. This creates a paper trail and deters aggressive verbal tactics.

- Explore Resolution Options: Discuss loan restructuring, settlement options, or other repayment plans with the bank.

- File Complaints: If harassment persists or becomes illegal, file formal complaints with the bank’s grievance redressal unit, the RBI Ombudsman, or the police (Cybercrime Cell for digital harassment).

- Seek Legal Protection: Do not hesitate to consult legal experts specializing in bank harassment. They can guide you, draft legal responses, and represent you if needed.

The Bank Harassment Advantage: Your Guide to Proactive Action

Ignoring bank harassment is a natural but dangerous response. At Bank Harassment, we transform that fear into empowerment:

- Consequence Clarity: We educate you on the potential consequences of ignoring harassment, helping you make informed decisions.

- Strategic Engagement: We guide you on how to effectively communicate with banks and recovery agents, ensuring your borrower rights are respected.

- Comprehensive Legal Protection: From advising on initial responses to assisting with formal complaints and legal action, we provide the legal protection necessary to resolve the issue effectively.

- Restoring Peace of Mind: By taking proactive action, you regain control of your situation, reducing mental stress and moving towards a sustainable resolution.

Don’t let the fear of bank harassment lead you to ignore the problem. Proactive action is not just about avoiding worse consequences; it’s about asserting your rights and finding a path to peace of mind.

If you’re facing bank harassment and are considering ignoring it, Contact Us at Bank Harassment today to understand your options and gain the legal protection you need for effective proactive action.