When overwhelmed by debt and under pressure from relentless Bank Harassment, borrowers often find themselves considering two main pathways to becoming debt free: Debt Settlement (negotiating a reduced payment) or formal Insolvency (a legal declaration of inability to pay debts).

Both options offer a way out of financial crisis, but they carry vastly different processes, consequences, and long-term impacts, particularly regarding your exposure to harassment and your future financial life. Choosing the right path depends entirely on the severity of your debt and your goals for future financial recovery.

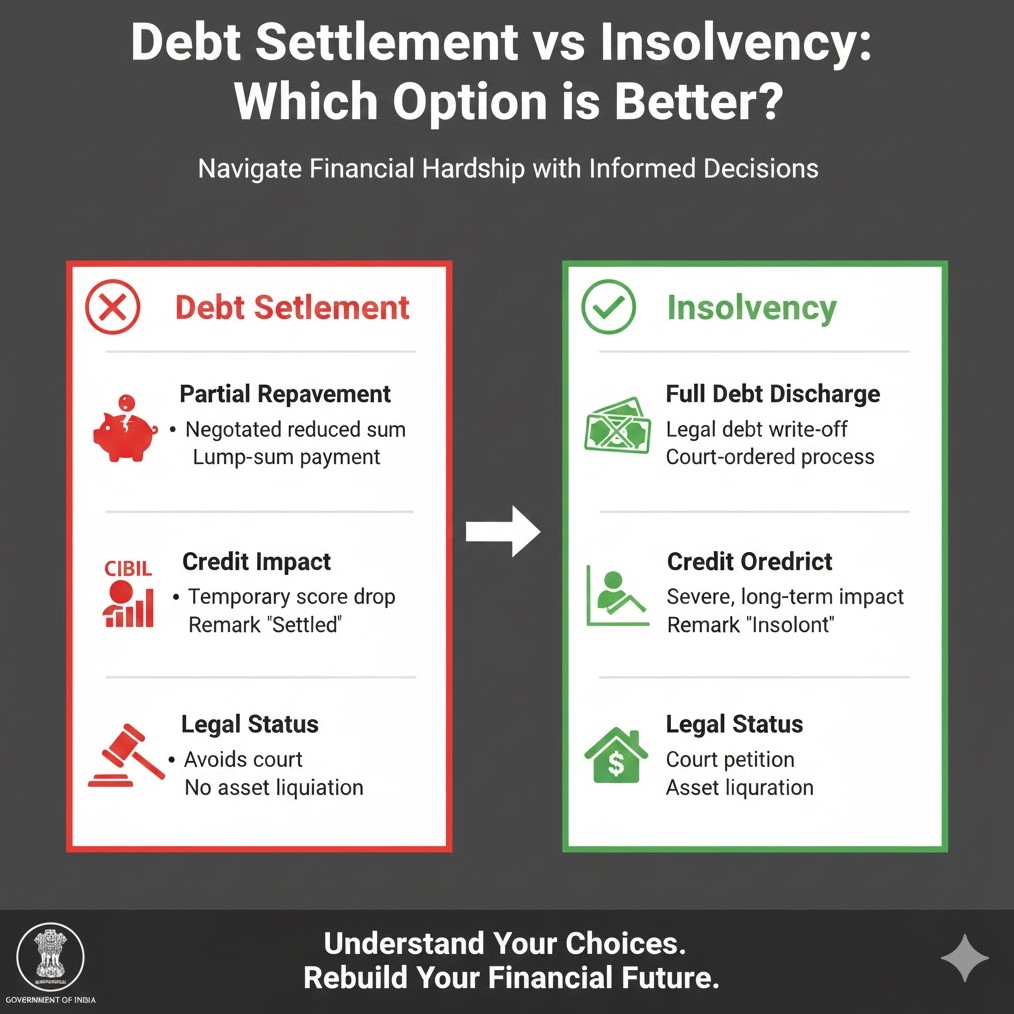

1. Debt Settlement (The Negotiation Route)

Debt Settlement is a negotiated agreement where you pay a single, reduced lump sum to the lender, who then agrees to waive the remainder. It is a tactical move for borrowers who want to close the debt quickly.

✅ When Debt Settlement is Better (Stopping Harassment Faster):

-

Speed & Control: This is the fastest route to becoming debt free. Once the final payment is made and the No Dues Certificate (NDC) is issued, the bank immediately loses all legal grounds for collection or Bank Harassment.

-

Assets: You maintain control of your high-value assets (like your primary residence or car).

-

Severity of Debt: Your debt is manageable but significant (e.g., 5-10 times your annual income), and you can arrange a lump sum payment (typically 40% to 70% of the principal outstanding) through family support or asset liquidation.

-

Credit Impact: The “Settled” status on your credit report is a severe negative marker, but it is generally considered less devastating than the “Insolvency” status, allowing for a quicker financial recovery over the long term.

❌ Drawbacks:

-

Requires arranging a large, immediate lump sum payment.

-

The bank may initially refuse to negotiate or demand an unfavorable settlement value.

2. Insolvency (The Legal/Court Route)

Insolvency (or bankruptcy) is a formal legal status declared by a court (NCLT/DRT in India) when an individual is unable to pay their debts. The process is governed by the Insolvency and Bankruptcy Code (IBC).

✅ When Insolvency is Necessary/Better (The Nuclear Option):

-

Severity of Debt: Your debt is absolutely unmanageable (e.g., 20+ times your annual income), and you have no realistic way to arrange any lump sum payment for settlement.

-

Immediate Halt to Legal Action: Formal insolvency proceedings immediately halt all recovery and legal actions against you, including foreclosure proceedings, offering an instant stop to the most aggressive forms of Bank Harassment.

-

Statutory Discharge: Insolvency can lead to a formal “discharge,” where the court legally frees you from all remaining eligible debts.

❌ Drawbacks:

-

Credit Impact: The “Insolvency” status on your credit report is the most severe negative marker, lasting up to seven years and making future borrowing virtually impossible during that time.

-

Loss of Control: The process is managed by a Resolution Professional, and you lose control over your financial affairs.

-

Loss of Assets: Your assets (except those legally protected) may be seized and liquidated to pay creditors.

-

Long Process: The legal process is lengthy, often taking months or even years.

Making the Final Decision

| Feature | Debt Settlement | Insolvency |

| Process | Private negotiation with the bank. | Formal legal/court proceeding. |

| Time Frame | Weeks to a few months. | Months to a few years. |

| Key Requirement | Ability to arrange a lump sum payment. | Debt is absolutely overwhelming (no lump sum possible). |

| End of Harassment | Immediate upon payment & NDC issuance. | Immediate upon court declaration/notice. |

| Control Over Assets | Maintain control over assets. | Assets are surrendered/liquidated. |

If you can arrange the lump sum—even by borrowing from family or selling a non-essential asset—Debt Settlement is almost always the preferred route due to its speed, lower long-term credit impact, and preservation of assets. It is the quicker, cleaner way to get debt free.

If the debt is truly insurmountable and you cannot arrange any funds for a settlement, Insolvency may be your only legal option to become debt free and stop further legal action.

Which path is right for your financial situation?

Contact Us today for a confidential consultation to assess your debt level and determine the optimal strategy for your financial recovery and freedom from Bank Harassment.