When drowning in high-interest Credit Card debt, the offer of a Loan Settlement (paying a reduced, lump-sum amount) feels like a necessary lifeline—especially when accompanied by the stress and fear of relentless Bank Harassment.

The core question is: Is Credit Card Settlement a safe or wise option?

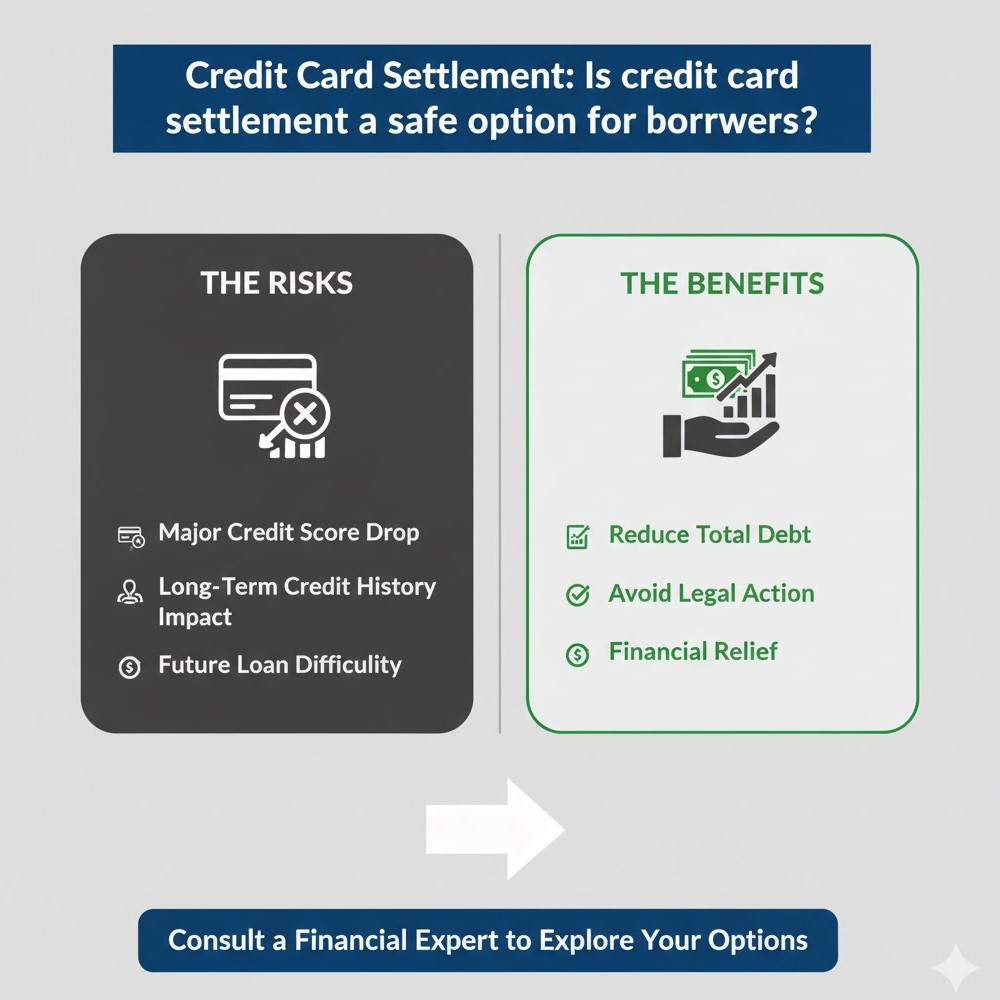

The truth is, it is a legally safe tool for debt elimination, but it is not a financially safe option and should only ever be treated as a definitive last resort to avoid total financial collapse.

1. How Settlement Offers Safety and Stops Harassment

In the face of aggressive debt collection, a properly executed Credit Card Loan Settlement provides safety in two crucial ways:

- Legal Finality: Once the negotiated lump sum is paid and you receive the bank’s Settlement Letter, the debt is legally extinguished. The bank cannot pursue you for the remaining waived amount (principal, interest, or penalties). This closure ends the bank’s legal mandate to pursue the debt.

- Stops Agent Harassment: The legal closure of the account instantly removes the debt from the recovery agent’s file. Your most powerful defense against continued Bank Harassment is the Settlement Letter, which proves to the bank that the account is closed and any further collection efforts are illegal and subject to RBI complaint.

Crucial Safety Precaution: NEVER pay the settlement amount based on a verbal agreement. Always demand a formal, written Settlement Letter on the bank’s official letterhead, explicitly stating the payment is in “Full and Final Settlement.”

2. The Major Risk: The 7-Year Black Mark

While a settlement stops Bank Harassment and closes the debt, it creates severe, long-term consequences for your financial future. This is the reason it is not a “safe” primary choice.

- The “Settled” Status: Your credit report will display the account status as “Settled” instead of “Closed” or “Paid in Full.” This signals to every future lender that you failed to meet your full contractual obligation.

- Massive Score Drop: Your Credit Score (CIBIL, Experian, etc.) will suffer a significant drop, often by 75 to 150 points or more.

- 7-Year Stigma: This highly negative “Settled” status remains visible on your credit report for up to seven years from the date of settlement.

- Future Loan Rejection: For that entire period, securing new unsecured credit (Personal Loans, other Credit Cards) will be extremely difficult, or the interest rates offered will be exorbitant due to your high-risk status.

| Account Status | Indication to Lenders | Impact on Future Credit |

| Closed/Paid in Full | Excellent credit behaviour. | Positive, easy access to credit. |

| Settled | Inability to repay debt in full. | Highly Negative. Expect rejection or high rates for 7 years. |

3. Options to Explore Before Settlement

Because of the extreme damage to your Credit Score, settlement should only be the choice when all other viable options to manage debt have failed:

- Debt Consolidation Loan: If your credit score is still functional, take a personal loan (at a much lower interest rate than the 30-40% charged by credit cards) to pay off the credit card debt in full. This prevents the “Settled” mark.

- EMI Conversion: Ask the card issuer to convert your outstanding balance into a fixed-tenure, fixed-interest Equated Monthly Installment (EMI) plan. This stops the vicious compound interest.

- Restructuring: Negotiate an interest rate reduction or an extension of the repayment period instead of a full settlement.

The Final Verdict:

A Credit Card Settlement is the most effective and legally secure way to eliminate debt and stop Bank Harassment. However, it comes at the high cost of your creditworthiness for up to seven years. Only use it when the short-term relief is absolutely necessary to prevent a financial catastrophe.

Are you facing aggressive Bank Harassment and need help determining your best option—consolidation or settlement?