When facing a default on a Car Loan, the idea of requesting a Loan Settlement (One-Time Settlement or OTS) is a strategic move to clear the debt. However, because a car loan is a secured loan—meaning the vehicle is the collateral—the threat of Bank Harassment and physical repossession remains intense.

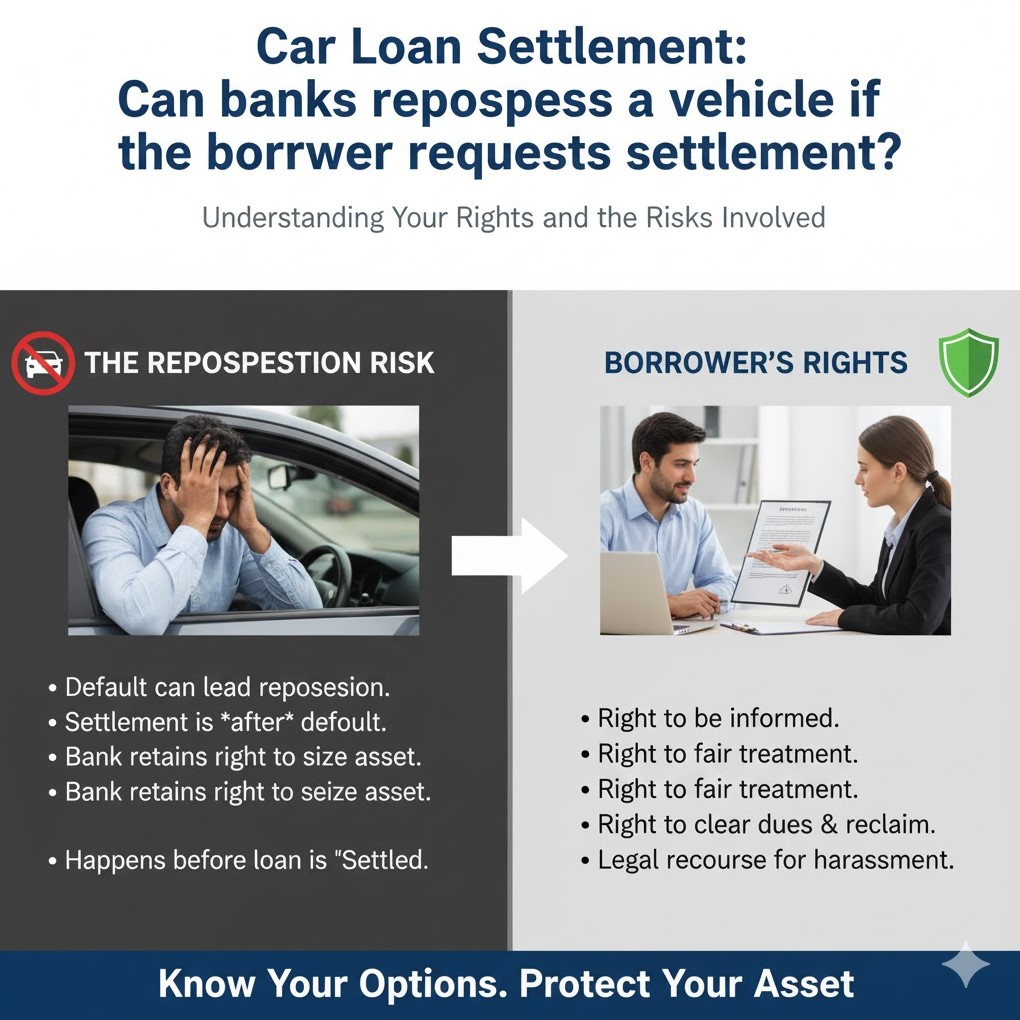

The hard truth is Yes, the bank retains the legal right to repossess your vehicle even if you request a settlement, if you are already in default. Your request for a settlement, by itself, does not legally shield the asset. The goal of the negotiation is to secure a signed OTS agreement and deliver the cash before the bank executes the seizure.

1. The Bank’s Power: The Right to Repossess

The bank’s right to repossess is established in the original loan agreement, which includes a hypothecation clause allowing seizure upon default.

- Settlement is Not a Shield: When you request a Car Loan Settlement, you are negotiating for a new contract (the OTS agreement). Until that new contract is signed and the money is paid, the original loan agreement remains in force, and the bank retains the right to seize the vehicle as per the original terms.

- Leverage Tactic: Many banks will continue the repossession process (or the threat of it) during settlement talks because the imminent loss of the vehicle pressures the borrower to arrange the cash for the settlement quickly. This is often a form of Bank Harassment disguised as legal procedure.

2. Your Strategy: How to Protect Your Vehicle During Settlement Talks

The key is to proactively manage the situation and ensure the bank sees a guaranteed, profitable path forward without repossession.

A. Propose a Quick Lump Sum (OTS)

The bank’s primary incentive to pause repossession is the guarantee of immediate cash. When proposing a settlement, emphasize that the lump sum payment can be made quickly (e.g., within 7–15 days). This immediate recovery is cleaner and cheaper for the bank than repossession, which involves costs for agencies, storage, and auction.

B. Formalize the Pause in Repossession

When you begin serious settlement talks, demand that the bank issue a communication (via email or letter) confirming they will put the repossession process on hold until the settlement deadline. While this is not always granted, it creates a paper trail and holds the bank accountable to its internal process. You can use any violation of this agreement in an Agent Harassment complaint.

C. Negotiate a Voluntary Surrender

If you are unable to raise the settlement amount but are certain you cannot keep the car, you can negotiate a Voluntary Surrender. This is often preferable to forced repossession as it can eliminate or reduce the expensive repossession fees charged to your account, giving you a better base for negotiating the remaining Deficiency Balance after the sale of the vehicle.

D. Secure the Written Agreement

Crucially, never pay the settlement amount until you have the bank’s formal, written Settlement Letter. This document, which guarantees the debt will be closed in “Full and Final Settlement,” is the only legal proof that removes the bank’s right to the collateral and their claim on you.

A Car Loan Settlement is the best path to closing a secured debt with dignity, but you must act quickly and strategically. Your negotiation must be backed by a clear plan to deliver the cash before the bank can execute its repossession right.