If you are facing an unaffordable car loan, you are likely dealing with two major issues simultaneously: the fear of debt and the abuse of relentless Bank Harassment.

While securing a Car Loan Settlement stops the harassment and resolves the debt, many borrowers worry about the final piece of the puzzle: the impact on their CIBIL score.

At Bank Harassment, we believe that resolving your debt and ending the abuse must come first. Dealing with your CIBIL (or credit score) is the next, manageable step. Here is the honest truth about settlement and how to plan your recovery.

Priority #1: Stop the Harassment and End the Debt

Before you worry about your CIBIL score, you must address the immediate crisis:

- The Harassment: Continuous, illegal Bank Harassment is a threat to your mental health and professional life. A settlement agreement is the only definitive way to eliminate the bank’s legal reason for hounding you.

- The Debt: An unresolved, defaulted car loan is a massive, growing liability. It destroys your finances faster than any credit score drop.

A Car Loan Settlement is the decisive surgical cut needed to remove the toxic debt, secure your peace of mind, and immediately halt all collection pressure.

The CIBIL Reality: Why “Settled” is a Necessary Step

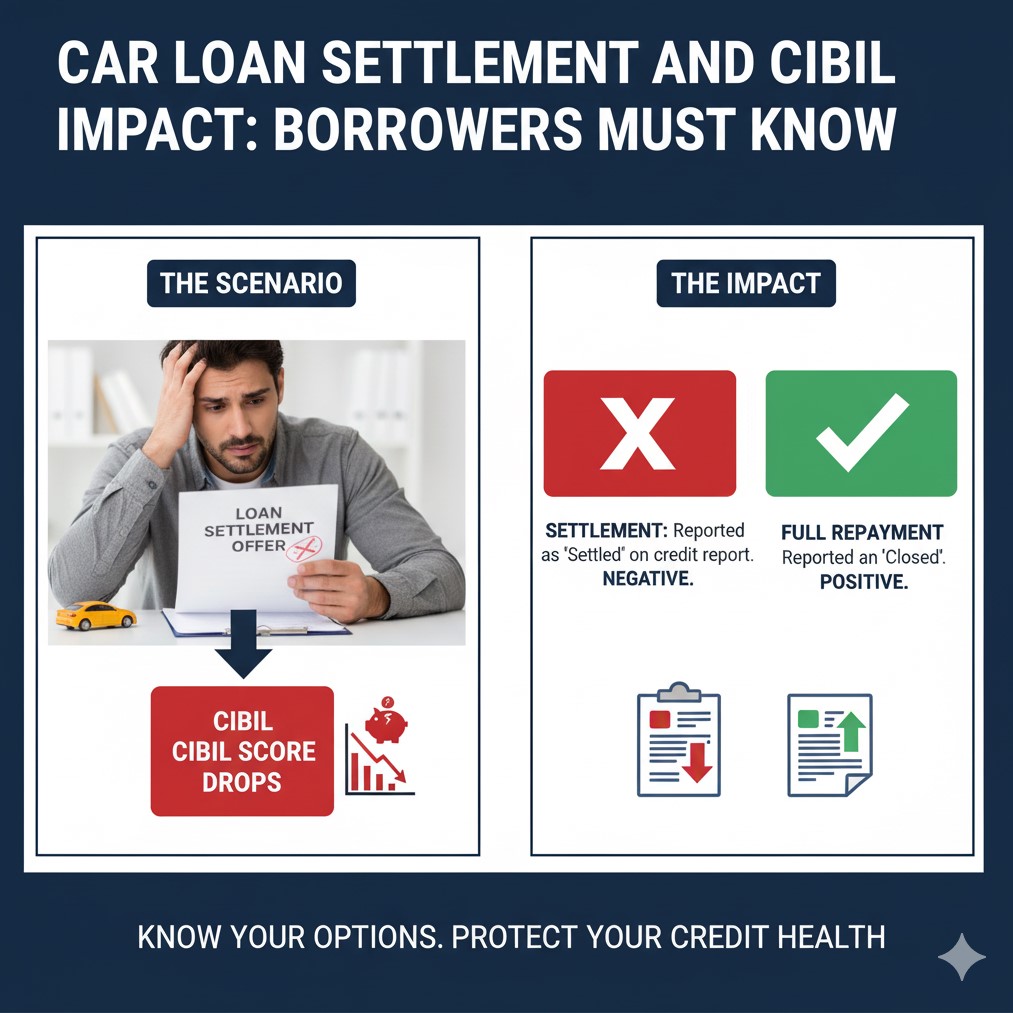

Any compromise on a loan is reported to the Credit Information Bureau (India) Limited (CIBIL) and will affect your credit score.

The Bottom Line: A temporary drop in your CIBIL score is the price of freedom. An open default, driven by the stress of Bank Harassment, is financial suicide. By settling, you take a necessary short-term hit for long-term stability.

Our Post-Settlement CIBIL Recovery Plan

Our work doesn’t end when the harassment stops. We set the stage for your financial recovery:

1. Ensuring Accurate Reporting

After your Car Loan Settlement is paid, we ensure the bank issues a No Due Certificate and reports the status correctly as “Settled Account” to CIBIL. We actively monitor your report for several months to correct any errors, such as the bank mistakenly reporting the account as “Written Off,” which is often worse.

2. Using Harassment as Leverage

We use the illegal Bank Harassment you’ve endured not only to secure a maximum debt reduction but also to push for clean documentation. Banks know their violations are illegal and often cooperate fully on the final paperwork to avoid further legal scrutiny.

3. Starting Your CIBIL Repair

Once the “Settled” tag is correctly applied, you can begin the recovery process:

- Focus on Secured Credit: Start with small, secured loans or credit cards to build a new, positive payment history.

- Zero Defaults: Ensure all future payments (utility bills, small new loans) are flawless.

- Time Heals: The impact of the “Settled” tag will gradually lessen over the next 2-3 years as your positive payment behaviour is recorded.

Take Control of Your Future Today

Don’t let the fear of a temporary CIBIL score drop keep you trapped in debt and under the thumb of Bank Harassment. Securing a Car Loan Settlement is the definitive, powerful first step toward a debt-free life.