When you’re facing severe financial difficulty and dealing with the constant fear of Bank Harassment, every loan feels the same—an urgent problem that needs solving. The good news is that Education Loans can absolutely be settled in a manner similar to Personal Loans and Credit Card debt.

However, the key to success is using the unique characteristics of the education loan to your advantage, especially when negotiating with a bank to stop agent intimidation.

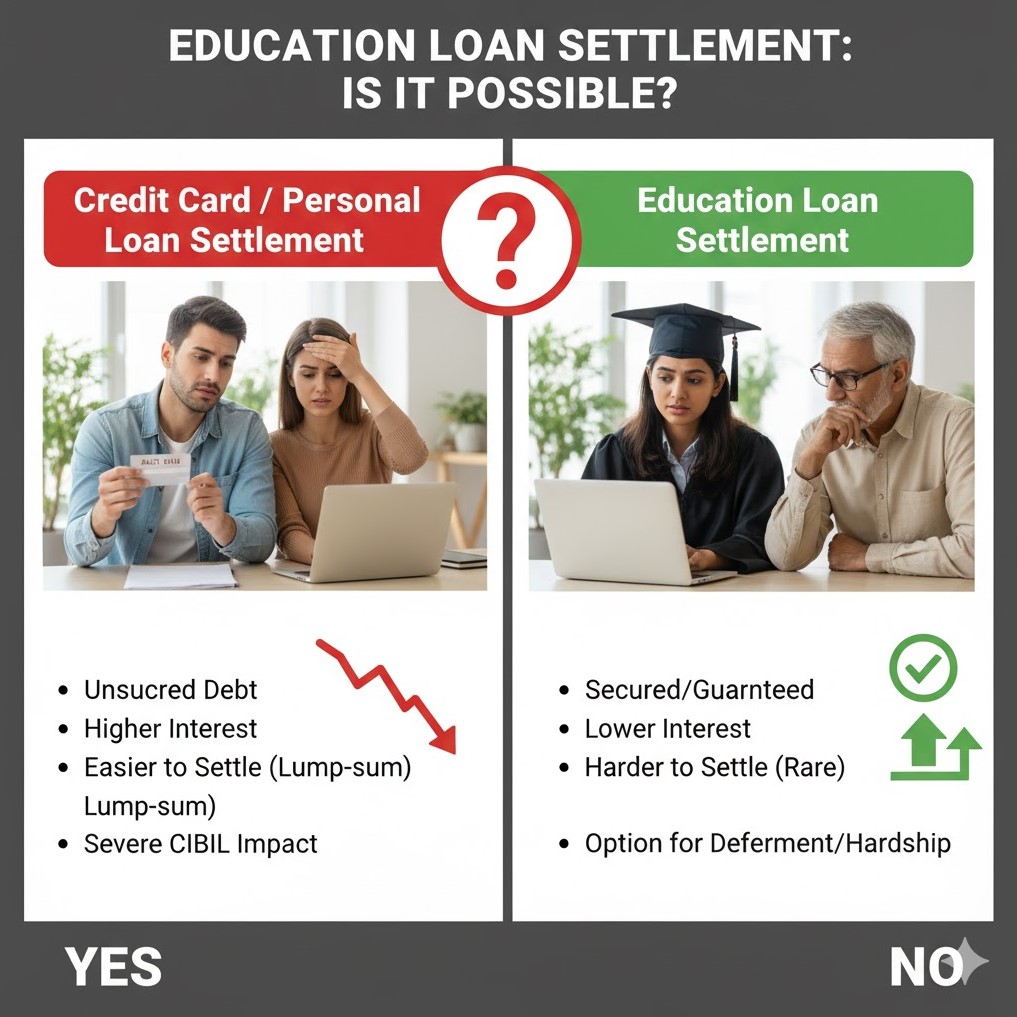

1. The Similarities: Why Settlement is Possible

The bank’s motivation for offering an Education Loan Settlement mirrors its reasons for settling any unsecured debt:

- NPA Resolution: Like a Personal Loan, if your Education Loan is past due for 90 days, it becomes a Non-Performing Asset (NPA). The bank is incentivized to recover a reduced amount now rather than allocate more capital against the loss.

- One-Time Settlement (OTS) Process: The negotiation process is identical: you propose a reduced, lump-sum payment (the OTS amount) to close the entire outstanding debt.

- Legal Clarity: A successful settlement, just like any other Loan Settlement, results in a legally binding contract that extinguishes the bank’s right to future claims and halts all legal recovery attempts.

2. The Key Difference: Your Stronger Leverage

Unlike a Personal Loan, which is based on the borrower’s current income, an Education Loan is a future-based risk for the bank. You can use this fact to gain leverage when negotiating and fighting Bank Harassment.

| Factor | Education Loan Settlement Leverage |

| Unemployment/Underemployment | If you are genuinely unemployed after graduation, you have strong documentation of hardship. This undercuts the bank’s aggressive tactics and proves settlement is the only viable path. |

| Moratorium Period | The RBI mandates a grace period for education loans (Model Education Loan Scheme). If default occurs immediately after this, the bank is more sensitive to a lack of career opportunity as the cause of default. |

| Co-Borrower Pressure | If your parents/relatives are co-borrowers, a settlement is often the fastest way to relieve their financial and psychological burden, making them more motivated to secure the settlement funds. |

| RBI’s Stance | The RBI guidelines encourage banks to facilitate loan restructuring for students facing financial constraints, such as extending the repayment period. If restructuring fails, settlement becomes the next logical, good-faith step. |

3. Using Settlement to Stop Bank Harassment

When agents harass you, they are betting on fear and intimidation. A formal, well-documented settlement proposal shifts the power dynamic immediately.

- Immediate Engagement: Stop ignoring calls and legal notices. Contact the bank’s recovery department and formally state your intention to propose an Education Loan Settlement.

- Documented Hardship: Submit comprehensive proof of unemployment (job search records, co-borrower financial statements). This documentation justifies the settlement and makes continued Bank Harassment unjustifiable and reportable under RBI guidelines.

- Secure the Letter: Once the settlement is agreed upon, the single most powerful tool is the written Settlement Letter. This document is your proof that the debt will be closed. Once paid, the bank’s mandate to the recovery agent ends instantly.

Don’t let Bank Harassment dictate your financial future. Your Education Loan may have unique challenges, but it also provides unique leverage for a successful settlement.

Ready to find a practical solution for your Education Loan and put an end to harassment?