A successful Loan Settlement is the victory that ends the debt cycle and stops the fear of Bank Harassment. But it comes with a major cost: the “Settled” status on your credit report (CIBIL, Experian, etc.). This negative entry drags down your Credit Score and casts a long shadow over your financial future.

Many borrowers ask: Does this damaging status automatically disappear after a few years?

Here is the definitive answer regarding the longevity of a “Settled” loan status and the strategic steps you can take to remove it before the mandated period ends.

1. The Reality: The 7-Year Rule

Under the regulations governing Indian credit bureaus, negative repayment entries like a Loan Settlement are designed to remain visible for a long period to ensure future lenders are fully aware of your past financial performance.

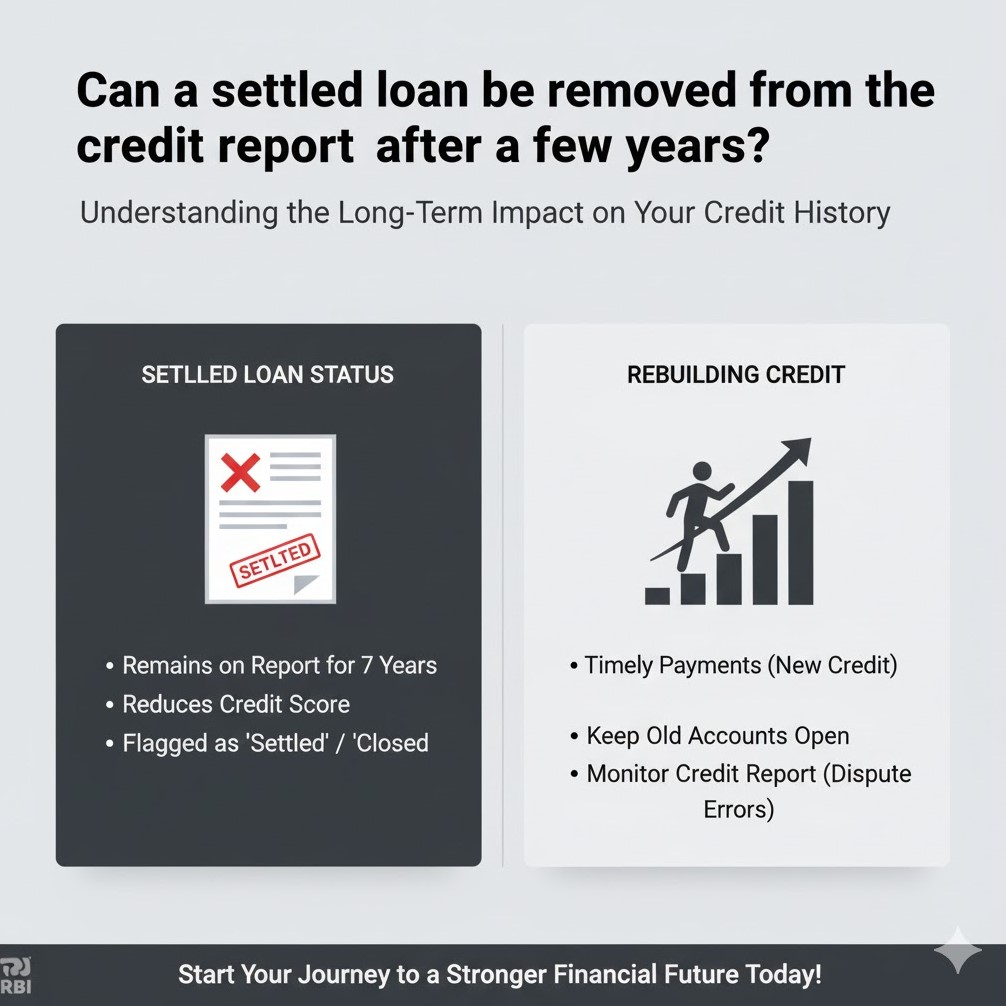

- Longevity: The “Settled” status typically remains on your credit report for up to seven years from the date the account was reported as settled (or sometimes, from the date of the first missed payment that led to the default).

- The Damage: For the entire seven years, the “Settled” tag acts as a severe red flag, significantly lowering your Credit Score and making it extremely difficult to obtain new loans, credit cards, or competitive interest rates.

- Automatic Removal: Only after this seven-year period concludes will the entry automatically drop off your report, and the negative impact will be fully removed.

2. The Solution: Converting “Settled” to “Closed”

You do not have to wait seven years! There is one powerful, strategic step you can take to legally remove the negative “Settled” mark much sooner: paying the waived-off amount.

| Status | Meaning | Impact |

| Settled | You paid less than the full, contractual amount. | Highly Negative. Remains for 7 years. |

| Closed/Paid in Full | You paid the full contractual amount. | Positive. Helps rebuild your score faster. |

The Strategic Process to Change the Status:

- Contact the Lender: Approach the bank or financial institution with whom you settled the loan. This is best done after you’ve stabilized your finances (e.g., 2-3 years after settlement).

- Request the Waived Balance: Formally request a statement detailing the exact amount that was waived off during the original settlement (the principal and interest that was written off).

- Negotiate and Pay: Offer to pay this entire remaining waived-off balance as a new lump sum. Frame it as the final step to resolving the full contractual liability.

- Demand the Status Change: Once the full, original debt amount is finally cleared, the bank is obligated to update the status on your credit report from “Settled” to “Closed” or “Paid in Full.”

- Obtain the New NDC: Secure a new No Dues Certificate (NDC) confirming the loan is now fully cleared based on the full contractual amount.

- Dispute with CIBIL: If the bank is slow to update the status, raise a formal dispute with the credit bureau (CIBIL/Experian), attaching the new NDC as proof of full repayment.

This action immediately removes the most damaging aspect of your credit history, providing a huge boost to your Credit Score and accelerating your recovery process by years. It’s the final step in truly closing the chapter on debt and Bank Harassment.

Ready to start the process of converting your “Settled” loan status to “Closed” for faster credit recovery?