Dealing with debt is a stressful experience, but when that stress is compounded by aggressive recovery tactics, it can become unbearable. Many borrowers in India find themselves trapped between rising interest rates and the fear of the next phone call. If you are struggling to keep up with your EMIs and are facing constant pressure from lenders, understanding the Personal Loan Settlement process is the first step toward reclaiming your life.

A settlement is more than just a financial transaction; for many, it is the only way to stop Bank Harassment and find a path to being Loan Free. This guide explains how the process works and how you can navigate it while protecting your legal rights.

What Does it Mean to Settle a Personal Loan?

In the context of the Indian banking system, a settlement occurs when a bank or NBFC agrees to accept a lump-sum payment that is less than the total outstanding amount you owe. This typically happens after a loan has been in default for several months and the bank realizes that recovering the full amount is unlikely.

Once the agreed-upon amount is paid, the lender marks the loan as “Settled” and stops all recovery efforts. While this provides immediate relief from the cycle of debt, the Loan Settlement Process requires careful handling to ensure you are not intimidated into an unfair deal.

The Step-by-Step Personal Loan Settlement Process

Navigating a settlement requires patience and a clear understanding of your financial position. Here is the path to a successful resolution:

1. Document the Hardship

Banks do not offer settlements easily. You must prove that your inability to pay is due to a genuine crisis—such as a job loss, a medical emergency, or a failed business. Collect all relevant documents to build a strong case for Personal Loan Settlement.

2. Confronting the Harassment

During the default period, many borrowers face intense pressure. It is crucial to remember that RBI guidelines strictly prohibit recovery agents from using abusive language, calling at odd hours, or threatening physical harm. If you are being harassed, keep a record of these interactions. Platforms like Bank Harassment specialize in shielding borrowers from these illegal tactics, allowing you to negotiate from a position of strength.

3. Initiating the Negotiation

You can approach the bank’s credit or settlement department to express your intent to settle. The Loan Settlement Process involves finding a middle ground between what you owe and what you can realistically afford to pay as a one-time payment. In many cases, banks may waive a significant portion of the interest and penalties to help you become Loan Free.

4. Securing the Written Sanction

One of the biggest mistakes borrowers make is paying money based on a verbal promise from a recovery agent. Never pay without a formal Settlement Sanction Letter. This letter must be on the bank’s official letterhead and should clearly state the final settlement amount and the date by which it must be paid.

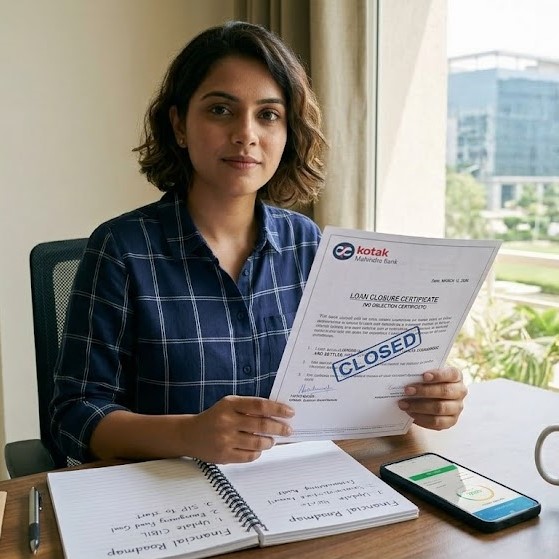

5. Payment and Formal Closure

After making the payment as per the sanction letter, ensure you receive a payment receipt and a confirmation that no further dues are pending. This prevents the bank from coming back later with additional demands and is the final step to being Loan Free.

The Reality of “Settled” Status

While a Personal Loan Settlement stops the calls and legal threats, it does impact your credit history. On your CIBIL report, the account will be flagged as “Settled” for several years. This indicates to future lenders that you did not pay the full amount, which may make getting new credit difficult in the short term. However, for those facing extreme mental and financial pressure, the immediate peace of mind and the end of Bank Harassment are often worth the temporary dip in creditworthiness.

Why You Need a Legal Shield

Banks and NBFCs have vast resources and experienced recovery teams. As an individual, you might feel pressured to sign documents you don’t understand or agree to payment terms that are impossible to meet. Seeking professional help through Bank Harassment ensures that you have experts who understand Indian banking laws and RBI guidelines. They can stop the bullying and negotiate a fair settlement that actually fits your financial reality.

Conclusion

Debt should not cost you your dignity. The Loan Settlement Process is a legal way to resolve your financial burdens when life takes an unexpected turn. By standing up for your rights and following a structured approach, you can put an end to the harassment and start your journey toward a Loan Free future.

To learn how to protect yourself from aggressive recovery tactics and find a permanent solution to your debt, visit Bank Harassment today.