When you’re overwhelmed by debt and under constant pressure from Bank Harassment, choosing a Loan Settlement Company is a crucial decision. A genuine partner acts as your legal firewall and strategic negotiator; a fraudulent one can leave you poorer and more vulnerable.

The debt relief market in India is unregulated by the RBI, making vigilance essential. To secure your borrower protection and a safe debt closure, you must know how to distinguish a genuine trusted partner from a scam.

1. Verify Legal Registration and Expertise

A legitimate company should have a verifiable legal structure and qualified staff.

-

Check Corporate Identity: A genuine company is usually registered as a Private Limited Company or LLP. Ask for their Corporate Identity Number (CIN/LLPIN). You can often verify this number on the Ministry of Corporate Affairs (MCA) website to ensure they are a legally incorporated entity.

-

Insist on Legal Advisors: The core of a settlement is negotiation and legal documentation. The company’s expert panel should clearly include experienced Legal Advisors or advocates specializing in banking, debt recovery, and consumer laws.

-

Verifiable Address: A reputable firm should have a professional website and a verifiable physical office address (not just a P.O. box or an online-only presence).

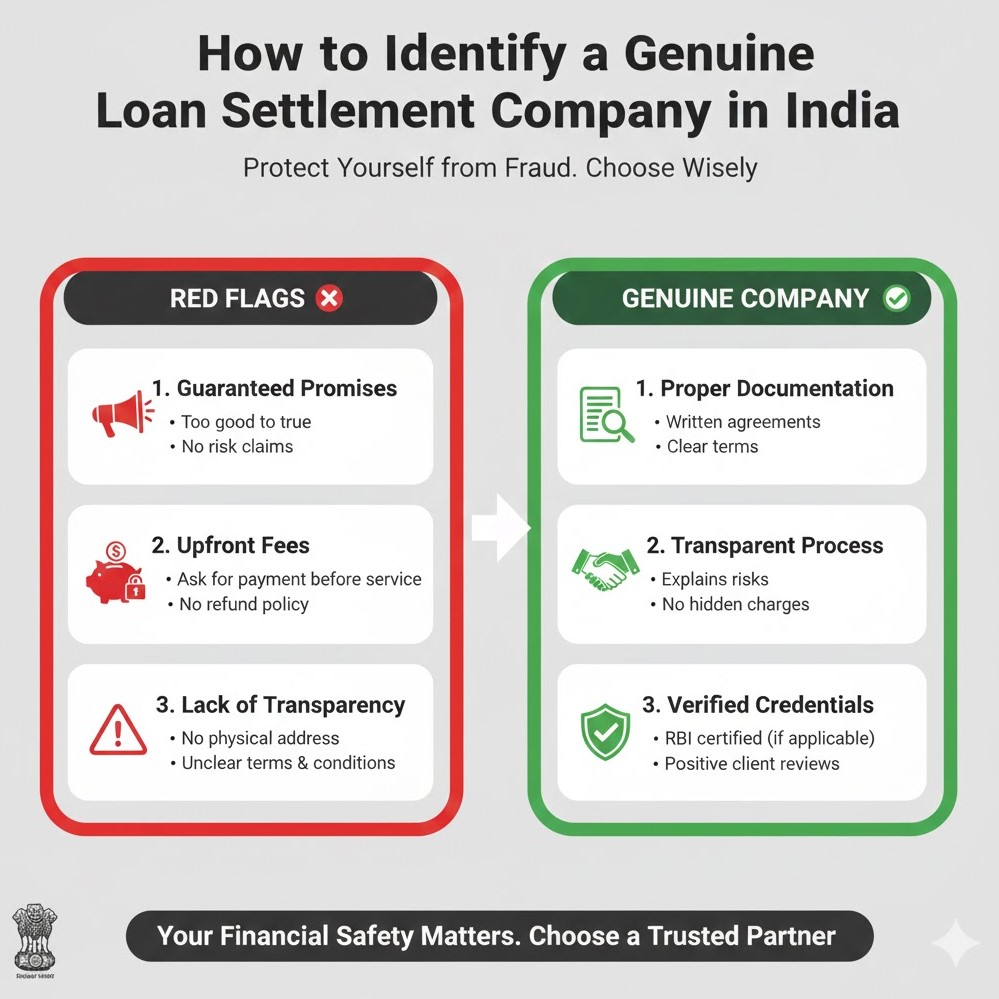

2. Red Flags: What Genuine Companies Never Do

Scammers use high-pressure tactics and make unrealistic promises. Treat any company displaying these behaviors as a major red flag:

| Red Flag Behavior | Why It’s Suspicious |

| Guaranteeing Results | They promise “100% debt reduction” or a fixed, low settlement value. No one can guarantee a specific settlement, as the final offer depends solely on the bank’s discretion. |

| Large Upfront Fees | Charging a large, non-refundable fee before any negotiation work has begun. Genuine firms typically use transparent, milestone-based, or success-based fees. |

| Asking for Login Details | NEVER share your bank account, credit card, or Net Banking login IDs/passwords. A genuine partner only needs account statements and authorization letters. |

| Promising CIBIL Clean-Up | They promise to “remove” the “Settled” status from your CIBIL report quickly. The status remains for up to 7 years; it cannot be legally removed before that time. |

| Handling Settlement Funds | They ask you to pay the final settlement lump sum into their company or a personal account. The lump sum must always be paid directly to the bank via DD or official bank transfer. |

3. Focus on Borrower Protection & Documentation

A trusted partner prioritizes your legal safety over a quick deal.

-

Communication as Firewall: A genuine firm will handle all communication with the bank and recovery agents on your behalf, effectively stopping the Bank Harassment. They document every call and threat to use as leverage in negotiations.

-

Documentation Priority: They should be obsessed with the Loan Settlement Letter and the No Dues Certificate (NDC). They act as your shield to ensure the bank delivers these critical legal documents upon payment, thereby ensuring true debt closure.

-

Clear Fee Contract: Insist on a written contract that clearly outlines the total service charges, the scope of services, and the payment schedule before you pay anything.

By choosing a partner who prioritizes ethical standards and borrower protection, you ensure that your path to debt freedom is secure, legal, and permanent.

Ready to partner with a trusted expert?

Contact Us today for a confidential assessment and begin your loan settlement journey with confidence and complete borrower protection, free from harassment.