When you are fighting aggressive Bank Harassment, the goal is to secure a swift and affordable loan settlement to permanently end the abuse. Negotiation is useless without a well-calculated, realistic number. You need to determine the maximum affordable amount you can offer while understanding the minimum amount the bank might accept.

Guessing or offering a random number will lead to a rejected bank offer. Using a calculated approach—like a mini loan settlement calculator—ensures your offer is taken seriously and maximizes your savings, helping you reach a swift resolution and peace of mind.

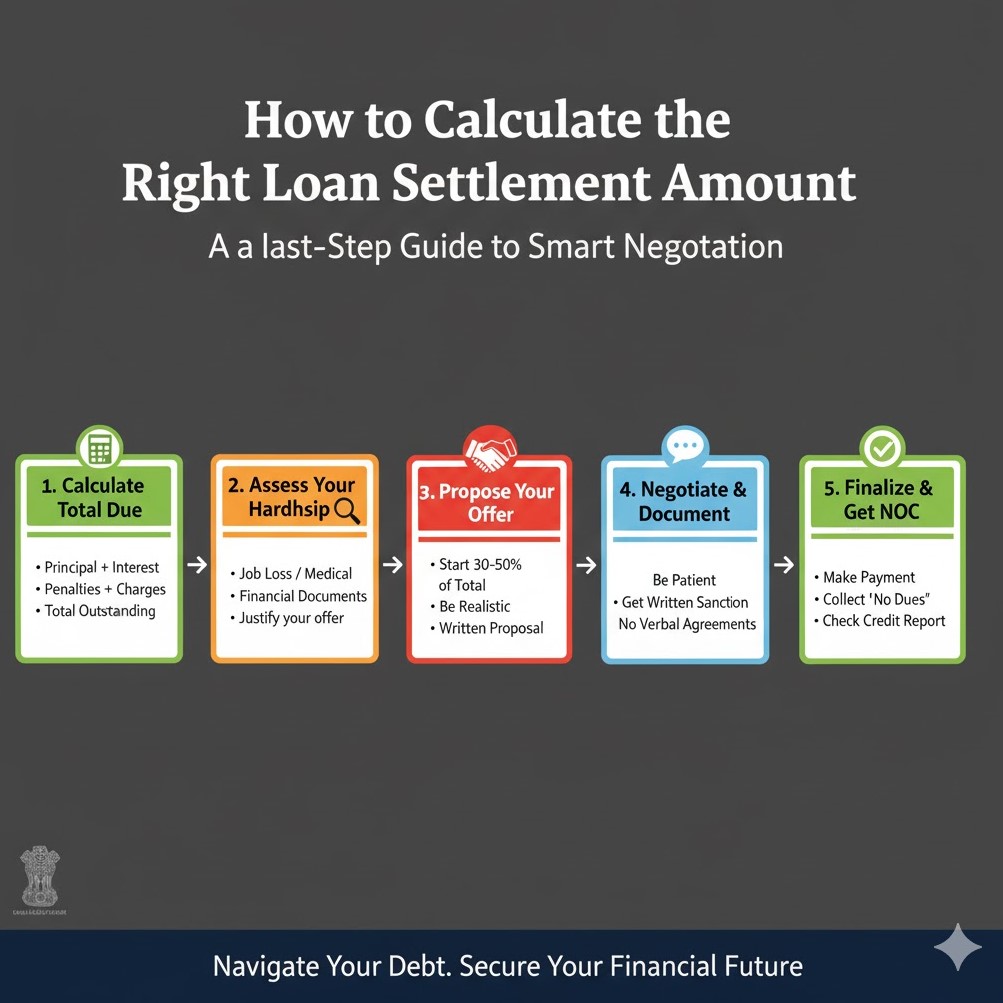

Step 1: Calculate Your True Outstanding Liability

Before you negotiate, you must know what the bank claims you owe versus what you actually want to offer. Get the latest loan statement (or request a detailed statement of account).

-

Principal Outstanding (PO): Get the latest statement showing the unpaid principal amount. This is the core debt.

-

Accrued Interest (AI): The interest that has accumulated since your last full EMI payment.

-

Penalties & Fees (PF): This includes late payment charges, legal fees, and administrative costs. This is the amount the bank is most likely to waive.

Example: If your Principal Outstanding is ₹5,00,000, Accrued Interest is ₹50,000, and Penalties/Fees are ₹1,00,000, your TOL is ₹6,50,000.

Step 2: Determine the Bank’s Likely Floor (The Baseline Settlement Value)

The bank is driven by recovery goals and the loan’s current status (NPA). They will settle to avoid the high cost of persistent harassment and potential legal fees.

-

Target: Banks usually aim to recover the Principal Outstanding (PO) plus a small portion of the unrecovered interest (AI). They are almost always willing to waive the high Penalties & Fees (PF) to close the account quickly.

-

Bank’s Floor Calculation: A conservative estimate for the bank’s minimum acceptable settlement value often falls between 60% to 90% of the Principal Outstanding (PO).

-

Using the example above (PO = ₹5,00,000): The bank’s minimum likely recovery target is ₹3,00,000 (60% of PO) to ₹4,50,000 (90% of PO).

-

Step 3: Calculate Your Maximum Affordable Offer

The most important number is the one you can actually pay. This is your personal loan settlement calculator.

-

Cash in Hand: How much cash can you access right now (savings, selling assets, family help)? This is your absolute maximum offer.

-

Offer Strategy: Your initial bank offer should be conservative—start low, slightly below the bank’s likely floor, to give you room to negotiate upward without exceeding your capacity.

| Your Calculation | Example Amount | Strategy |

| Your Max Capacity (Must Pay) | ₹3,50,000 | Never offer more than this. |

| Initial Offer (Start Low) | ₹2,50,000 (50% of PO) | Lowball to open negotiation. |

| Target Settlement Range (Aim Here) | ₹3,00,000 – ₹3,50,000 | The realistic zone where the bank may agree. |

Step 4: Finalizing the Offer

-

The Power of Lump Sum: Your offer is exponentially stronger if you can pay the agreed amount as a single, lump sum (One-Time Settlement or OTS). The guarantee of immediate cash recovery encourages the bank to accept a lower settlement value than if they had to manage a multi-month repayment plan.

-

Leverage the Harassment: If the bank counters too high, remind them (professionally) that continued collection efforts violate RBI guidelines and risk official complaints. Resolving the debt now, via your offer, is the fastest way for them to close the NPA and eliminate regulatory risk.

By performing this simple calculation before you contact the bank, you replace desperation with strategy, ensuring you secure the lowest possible settlement value that works for your finances and permanently ends the Bank Harassment.

Need help running your own Loan Settlement Calculator?

Contact Us today. Our experts can analyze your outstanding liability and help structure the perfect bank offer for a swift loan settlement.