A Loan Settlement is the final, decisive action that ends your debt cycle and stops the fear of Bank Harassment. While it grants immediate peace, it leaves a significant, long-lasting scar on your credit profile. Understanding the severity of this damage is crucial for planning your financial recovery.

1. The Harsh Reality: The Impact on Your CIBIL Score

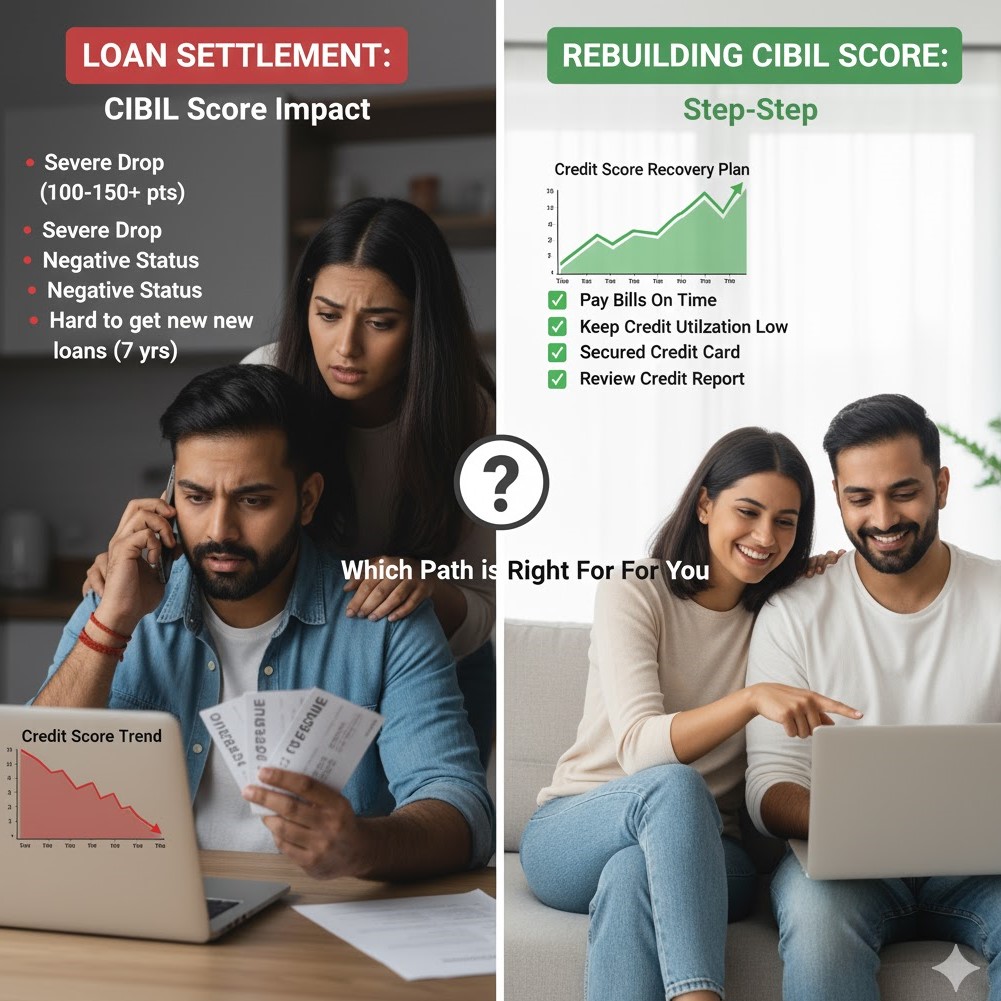

The core issue is the status the bank reports to credit bureaus (like CIBIL):

- “Settled” Status is a Major Red Flag: A loan marked as “Settled” means you paid less than the full contracted amount. This is viewed by lenders as a high-risk indicator—a failure to honor the original agreement. This status is far worse than a one-time late payment.

- Immediate and Severe Score Drop: A loan settlement causes an immediate and significant drop in your CIBIL Score, often between 75 to 150 points or more, depending on your credit history before the default.

- Long-Term Visibility: The negative “Settled” status remains visible on your credit report for up to seven years from the date of settlement. During this period, securing new loans (especially unsecured ones like credit cards or personal loans) will be extremely difficult, and any approved credit will likely come with much higher interest rates.

2. The Phoenix Strategy: 5 Steps to Repair Your Credit Score

Recovery is a marathon of discipline and patience. Follow this plan to strategically rebuild your creditworthiness.

Step 1: Verify and Correct the Record (The Foundation)

- Secure the NOC: After paying the settlement, immediately obtain the formal No Objection Certificate (NOC) from the lender. This is your proof of closure.

- Verify Status: Pull your current CIBIL Report. Ensure the settled loan shows a ₹0 Outstanding Balance and is correctly marked as “Settled.”

- Dispute Errors: If the status shows “Written Off” or any other incorrect detail, file a formal dispute with the credit bureau immediately. Correcting errors is the first step toward mitigation.

Step 2: Master Timely Payments (The Top Scoring Factor)

- Flawless Record: Pay all your remaining financial obligations (utilities, rent, any existing EMIs, and credit card bills) on or before the due date. Consistency and timely payments are the largest factor in your CIBIL Score.

- Set Autopay: Use automatic payments for minimum amounts to prevent accidental late marks.

Step 3: Utilize New Credit Wisely (The Rebuilding Tool)

- Secured Credit Card: If traditional credit is denied due to your low score, consider applying for a Secured Credit Card (backed by a Fixed Deposit). This allows you to use credit and build a positive payment history, as all activity is reported to CIBIL.

- Maintain Low Credit Utilization (CUR): Never use more than 30% of your available credit limit on any card. High utilization signals financial distress and severely hurts your score.

Step 4: Avoid “Credit-Hungry” Behaviour

- Limit Hard Inquiries: Do not apply for multiple loans or credit cards in a short period. Each “hard inquiry” temporarily lowers your score. Be selective and patient.

Step 5 (The Ultimate Fix): Convert “Settled” to “Closed”

- If your finances recover, you can approach the bank and offer to pay the remaining waived-off amount from the original loan. If the bank agrees, they can update the status on your CIBIL report from “Settled” to “Closed.” This instantly removes the most significant negative mark and provides a major, permanent score boost.

A Loan Settlement closed the door on debt and Bank Harassment. Now, focus on discipline and structure to methodically rebuild your credit profile and open the door to a secure financial future.

Ready to start your structured credit repair plan?