If you are reading this, you are likely overwhelmed—not just by debt, but by the relentless, often illegal, harassment from recovery agents. Every phone call, every unexpected visit, adds to the stress.

You know you need a way out, and two terms constantly surface: Debt Consolidation and Debt Settlement.

But which option actually brings the fastest and most complete relief from the collection calls? The answer depends entirely on your financial standing, and for most people facing harassment, the choice is clear.

Here is an honest, strategic breakdown of these two options through the lens of a borrower in crisis.

The Crucial Filter: Are You Stable, or Are You in Crisis?

Before you choose a strategy, you must be brutally honest about your current financial life.

1. Debt Consolidation: For the Stable Borrower

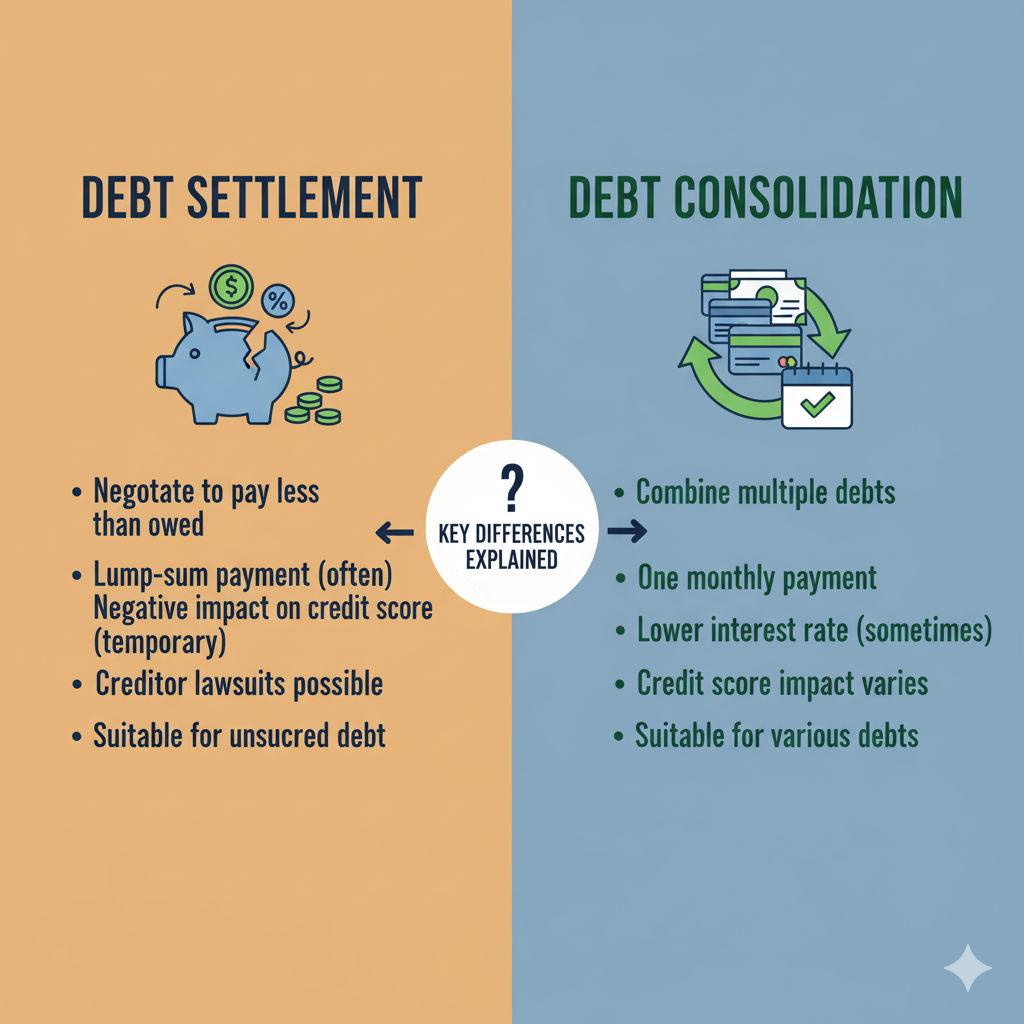

What it is: You take out a new loan at a lower interest rate to pay off all your high-interest debts (like credit cards). You combine 3-4 EMIs into one, simpler payment.

The Harassment Angle: Consolidation only works if you can qualify for a new, affordable loan.

- If you are NOT currently defaulting: Consolidation can work. Once the new loan pays off the old debts, the original creditors have been paid in full, and their collection calls should stop.

- If you are ALREADY defaulting: You will likely not qualify for a low-interest consolidation loan. If you take one at a high rate, you simply shift your debt—and your future harassment problem—to a new lender. This is not a viable option for most people facing bank harassment.

2. Debt Settlement: The Legal End to Harassment

What it is: A professional negotiation with your lender to pay a one-time, reduced lump sum (often 40%–60% of the principal) to close the account forever. You pay less than you owe.

The Harassment Angle: Settlement is the definitive, legal way to permanently end the collection process on a specific debt.

The moment the settlement amount is paid and the bank issues the final No Dues Certificate and Settlement Letter, the debt is legally resolved. The collection agency has no legal ground to pursue you for that specific account again.

For individuals facing severe, non-stop harassment, the goal is often immediate peace and a clean break, even if it comes at a cost.

The Strategic Choice: Peace Now vs. Future Credit

If you are facing bank harassment, you are likely in a situation where Debt Consolidation is simply out of reach or would only postpone the problem.

Your strategic decision boils down to this:

Your Legal Shield: Why Expert Intervention is Essential

The moment you hire an expert to handle your debt settlement, you gain an immediate layer of protection.

- Stop Illegal Calls: We step in as your legal representative. When a bank is notified that you are pursuing a legal settlement, most stop the illegal, harassing calls and visits immediately.

- Ensure Legal Closure: We negotiate the lowest possible settlement and ensure you receive the official Settlement Letter. This document is your ultimate shield against future collection attempts, legally confirming the debt is closed.

You do not have to endure illegal harassment. Your rights as a borrower are protected by RBI guidelines and Indian law.

If you are facing relentless collection calls and genuinely cannot repay your debt in full, Debt Settlement is your most powerful tool for immediate and lasting peace.

Don’t wait for the next call or threat. Consult with our legal experts today to understand how a strategic debt settlement can legally end the harassment and help you reclaim your life.