When you’re overwhelmed by debt and bank harassment, you’re constantly looking for a way out. You might be offered a loan top-up by your bank, or you might be considering a loan settlement.

But be warned: these are not two sides of the same coin. They are solutions for two completely different financial situations. Choosing the wrong one can lead you directly into a deeper debt trap and more intense harassment.

At Bank Harassment, we want to make it clear: a loan top-up is a dangerous trap, while a loan settlement is a strategic escape.

The Dangerous Illusion of a Loan Top-Up

A loan top-up is an additional loan on top of your existing one. It is designed for financially stable customers who have a good repayment history and need extra funds for things like home renovation, a medical emergency, or a child’s education.

A bank offers you a top-up because they see you as a low-risk borrower.

Why a Top-Up is a Dangerous Trap for a Stressed Borrower:

- It Adds to Your Debt: If you are already struggling to pay your EMIs, a top-up doesn’t solve your problem—it makes it worse. It gives you some quick cash but significantly increases your total debt burden and your new EMI.

- The Debt Spiral: Taking on new debt to pay off old debt is a classic symptom of a debt spiral. It will lead to more missed payments, more penalties, and, as a result, more aggressive harassment.

If a bank is already harassing you for a default, and they suddenly offer you a top-up, it’s a red flag. They are trying to get you to take on more debt so they can recover their money, but it will only deepen your crisis.

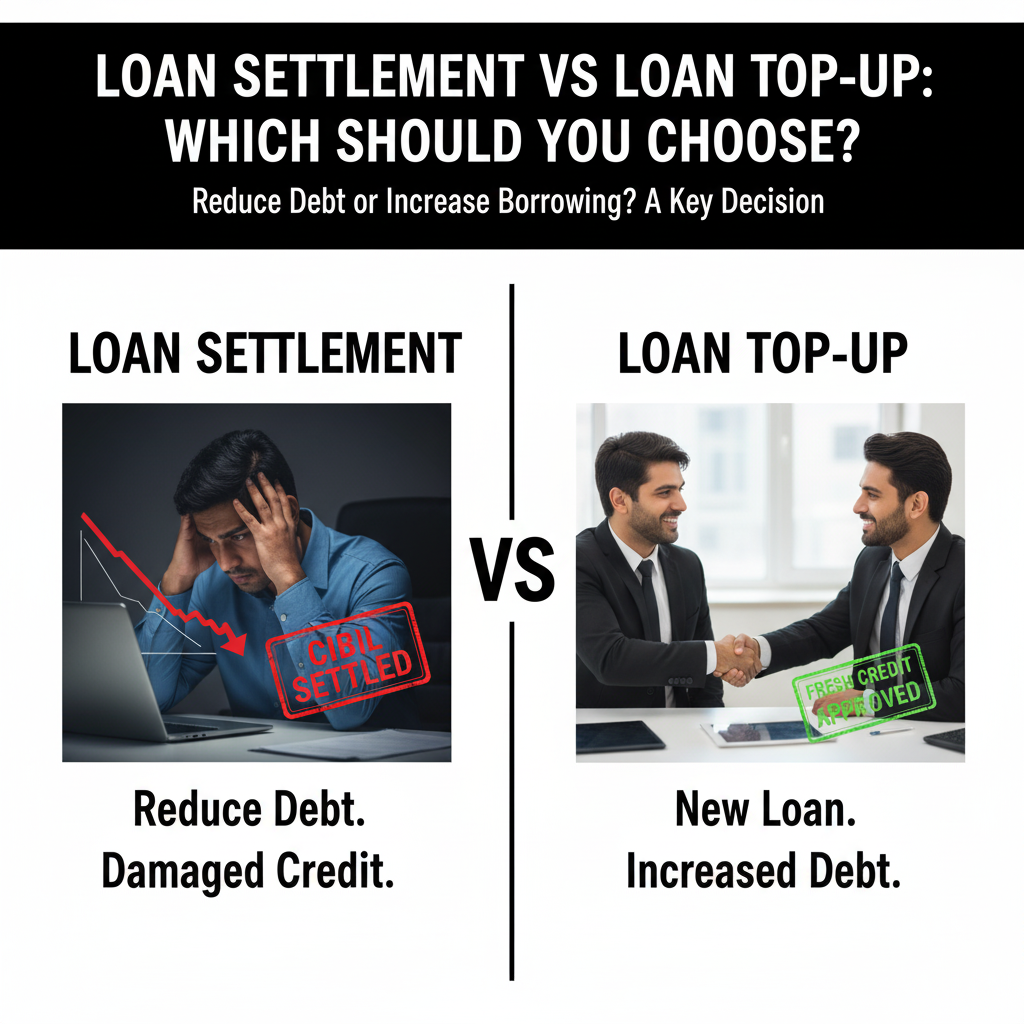

The Strategic Solution: A Loan Settlement

A loan settlement is a deliberate, negotiated agreement with your lender to close your loan by paying a lump-sum amount that is less than the total outstanding debt.

This is not for financially healthy people. It is a last resort for someone in severe financial distress who genuinely cannot repay their loan.

Why a Settlement is Your Strategic Escape from Harassment:

- A Legal End to Debt: A settlement provides a definitive, legal end to your debt. When you pay the agreed-upon amount, the bank has no legal right to pursue you for the remaining balance.

- Your Weapon Against Harassment: Once you receive a formal, written Settlement Letter and a No Dues Certificate (NDC) from the bank, any continued harassment from recovery agents is illegal. You can use these documents to file a complaint with the Banking Ombudsman or the police. The harassment stops because the debt is legally resolved.

- Avoids Total Catastrophe: While a settlement negatively impacts your credit score, it is a far better option than a complete default or bankruptcy. It allows you to close the chapter on your debt and begin to rebuild your financial life.

The Bottom Line: Which Path is Right for You?

The choice is simple, but it depends on your current reality:

- If you are financially stable and have a healthy credit score, a top-up loan can be a good option for a new project.

- If you are struggling with unmanageable debt and facing harassment, a loan top-up is a debt trap. A loan settlement is your only viable long-term solution to end your debt and stop the harassment for good.

Don’t let banks bully you into a bad decision. A settlement is not a sign of failure; it’s a strategic move to regain control of your life.

At Bank Harassment, we are experts in navigating the loan settlement process. We can help you negotiate with the bank, ensure you get the right legal documents, and provide you with the legal protection you need to permanently end the harassment.

Don’t add to your problems. Resolve them. Contact us today for a free consultation and let us help you find a strategic, legally sound path to a debt-free and peaceful life.